2019

48%

| DGL (Pacific) | Leading position and brand strength in the Pacific market |

|

|---|---|---|

| Growth capabilities leveraged by the Nippon Paint Group platform |

|

|

| Creating growth opportunities through an autonomous and decentralized management approach |

|

|

| DGL (Europe) | Established a leading position in the European decorative market through M&A |

|

| Leveraging market expertise from the Pacific for growth in Europe |

|

|

| Growth capabilities in the adjacencies market |

|

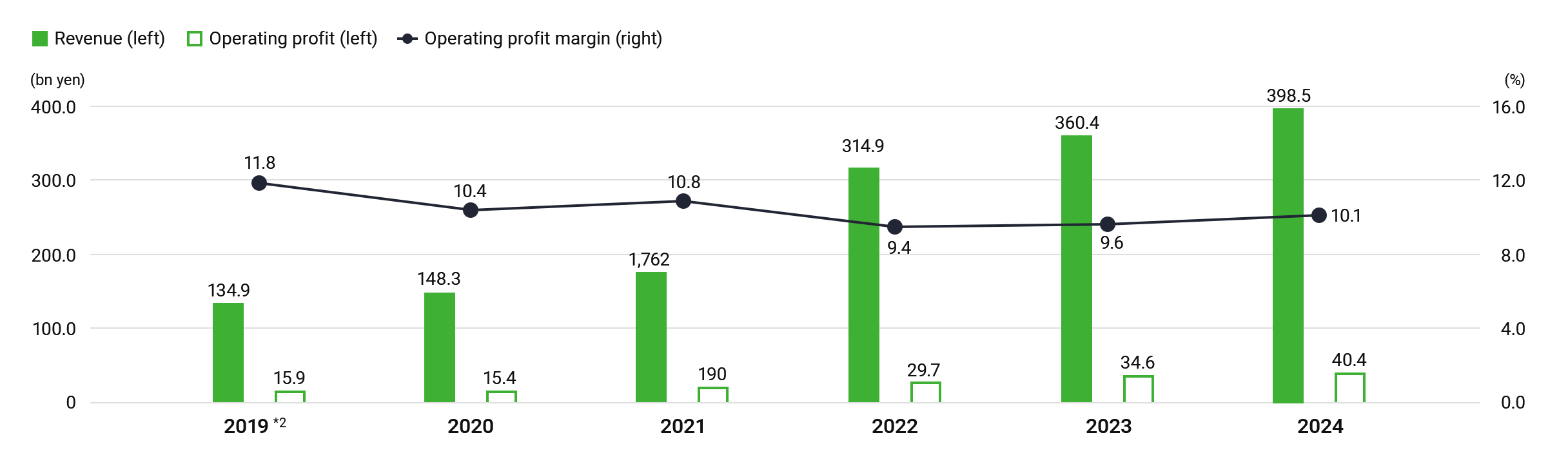

Revenue: In the decorative business, revenue increased year-on-year, despite sluggish sales volumes due to soft market conditions in the Pacific and Europe, partly driven by yen depreciation. In the adjacencies business, despite continued market weakness, revenue rose year-on-year, supported by business acquisitions in the Pacific region and the new consolidation of NPT. As a result, total revenue increased by 10.6% year-on-year to JPY 398.5 billion.

Operating profit: Despite higher SG&A expenses due to inflation, operating profit grew by 16.6% year-on-year to JPY 40.4 billion, supported by new consolidation, higher revenue, and an improved gross profit margin.

Under the guidance of its excellent management team, DuluxGroup has consistently achieved strong earnings growth through focus on organic and inorganic strategic growth initiatives across its three strategic pillars. DuluxGroup’s focus on strategic M&A has played an important role in complementing its organic growth initiatives, with over 30 acquisitions (including a mixture of strategic and small bolt-on businesses) executed since it joined Nippon Paint Group in 2019.

As a result, since the acquisition, revenue increased by 195.4% and operating profit rose by 153.9%.

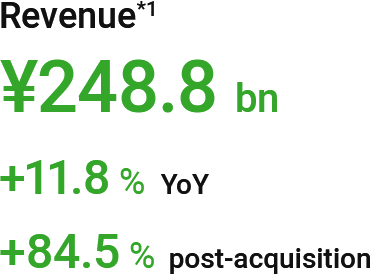

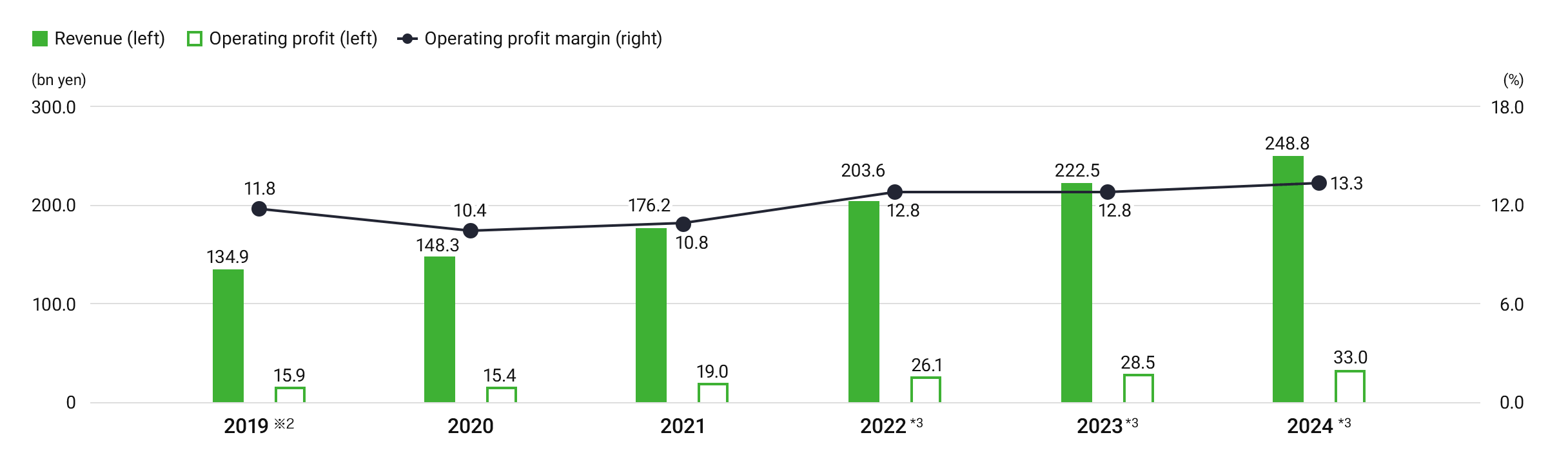

Revenue: Revenue from the decorative paints business increased from the previous year, despite the impact of soft market conditions, supported by price increases, an improvement in product mix, and yen depreciation. In the adjacencies business, revenue also rose, mainly driven by small-scale acquisitions of local businesses, which offset the impact of soft market conditions in existing businesses. As a result, total revenue grew by 11.8% year-on-year to JPY 248.8 billion.

Operating profit: Operating profit increased by 15.6% year-on-year to JPY 33.0 billion, driven by higher revenue despite higher SG&A expenses due to inflation.

Market share: DGL (Pacific) has maintained the No.1 market share in Australia for decorative paints, both in volume and value terms.

By relentlessly focusing on continuous investment in premium brand products, consumer insights, innovations, marketing, customer services catering to retail and trade-use customers, DuluxGroup has continued to outpace the market growth. Furthermore, the company has complemented its consistent organic growth with multiple strategic and bolt-on acquisitions.

As a result, since the acquisition, revenue has grown by 85.4% and operating profit rose by 107.5%.

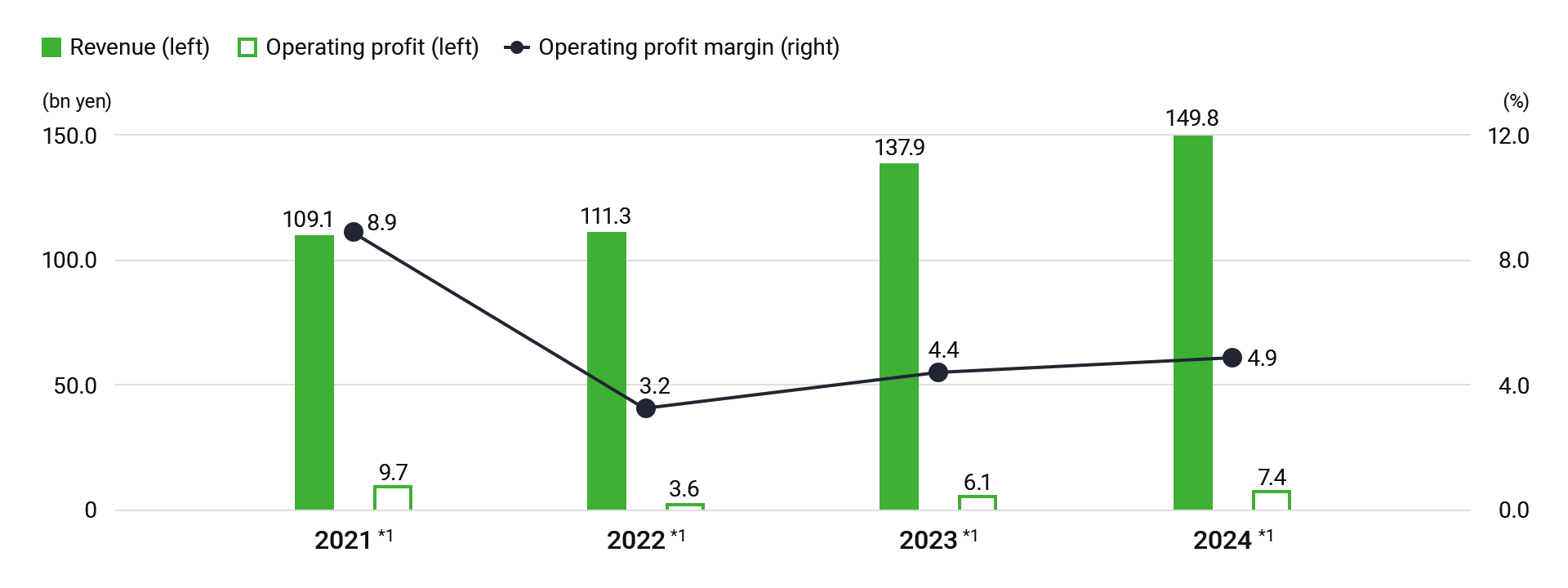

Revenue: Revenue from the decorative paints business increased year-on-year, despite sluggish sales volumes in France due to soft market conditions, supported by yen depreciation. In the adjacencies business, revenue also grew, as the impact of weak ETICS demand and a sluggish adjacencies market was offset by the new consolidation of NPT. As a result, total revenue rose by 8.6% year-on-year to JPY 149.8 billion.

Operating profit: Operating profit increased by 21.3% year-on-year to JPY 7.4 billion, supported by an improved gross profit margin and gains from the sale of the Craig & Rose factory, despite higher SG&A expenses due to inflation.

Market share: DGL (Europe) maintains a leading position in key European decorative paints markets, including Cromology’s No.1 market share in Italy and No.2 positions in France and Portugal, as well as JUB’s No.1 ranking in interior decorative paints in Slovenia, Croatia, Bosnia and Herzegovina, and Kosovo.

DuluxGroup is leveraging its core growth capabilities, developed through years of consistent expansion in the Pacific market, to accelerate growth, primarily through Cromology, the fourth-largest player in the European decorative paints market, and JUB, a leader in Central European decorative paint markets. Additionally, DuluxGroup is broadening its foundation in adjacency business through the acquisition of NPT, an Italy-based adhesives manufacturer.

As a result, since the time of acquisition, revenue has risen by 37.3%, with the consolidation of NPT offsetting declines in sales volumes in France.

Operating profit declined by 23.8%, primarily due to soft market conditions in France, M&A related expenses associated with NPT, and higher SG&A expenses driven by inflation.

| Cromology |

No.1 in Italy and No.2 in France (Trade only) and Portugal in decorative paints market

|

|---|---|

| JUB |

No.1 in Slovenia, Croatia, Bosnia and Herzegovina, and Kosovo in interior paints market

|

| DuluxGroup (Consolidated) |

|

|

|---|---|---|

|

|

|

|

| DGL (Pacific) |

|

|

|

|

|

|

|

|

|

|

| DGL (Europe) |

|

|

|

|

|

* Continued solar use in JUB and renewable power purchase in Cromology, though at reduced rate versus 2022 due to market pricing changes

For the SWOT analysis of each asset, please refer to the “Overview of Partner Companies” section in the Investor Book.