Features of the asset

-

- Driving our Group’s growth as the dominant No. 1 brand in the Asian paint market

- Steadily expanding the adjacencies business through group-wide collaboration and platform leverage

- Aiming to achieve both growth that outperforms the market and profitability through the expansion of market share in each region

-

- Gaining significant market share by capitalizing on the strong brand the company has built over the years

- Focusing on capturing repainting demand arising from the renovation of existing homes, a future growth area

- Aiming to expand market share particularly in Tier 3-6 cities, with the goal of becoming the market leader

-

- Leading the decorative paints market as the top brand in fast-growing Indonesia

- Delivering the highest profitability within our Group

- Striving to become the No. 1 market leader in decorative paints through strategies that fully maximize our brand strength

-

- Dominant No. 1 position in the Turkish decorative paints and ETICS markets

- Driving growth in the rapidly evolving market through a multi-brand strategy, leveraging strong brand power

- Aiming for sustainable growth by continuing the multi-brand strategy while expanding the range of SAF*, CC* and other adjacencies products

- SAF: Sealants, Adhesives & Fillers, CC: Construction Chemicals

Financial outcomes

-

2025 results

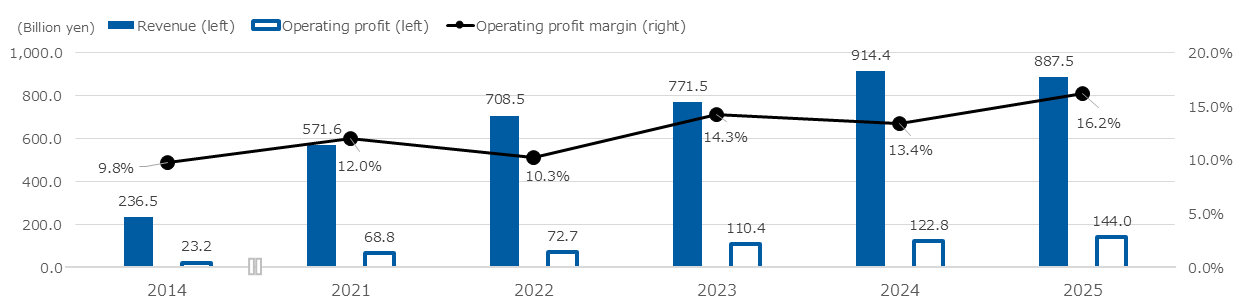

Revenue from automotive coatings in the NIPSEA segment increased compared with the previous year, as higher automobile production in China and strong sales to Chinese local automakers more than offset flat automobile production in Thailand. Revenue from decorative paints decreased, as increased sales volumes in China and key markets such as Malaysia and Singapore were offset by weak consumer sentiment and other adverse market conditions in other parts of Asia. As a result, consolidated revenue decreased by 2.9% year on year to ¥887,462 million, while consolidated operating profit increased by 17.3% to ¥144,021 million.

Growth since the acquisition (2014)

Since the consolidation in 2014, NIPSEA Group has driven our Group’s performance by achieving growth that significantly surpass market and competitors, leveraging its strengths: (1) exceptional brand strength, (2) top-notch talent cultivated through the LFG corporate culture, (3) robust production and distribution networks, and (4) strong technological capabilities. Additionally, by sharing with Betek Boya and PT Nipsea the extensive expertise and technologies accumulated over the past 60 years, NIPSEA Group has helped these acquired companies achieve higher growth post-acquisition. Furthermore, NIPSEA Group has steadily expanded its adjacencies business by deploying the Selleys brand of DuluxGroup and acquiring Vital Technical.

Consequently, compared to the time of acquisition, revenue has surged by 275% and operating profit soared by 521%.RevenueJPY 887.5 bnYoY -2.9%post-aquisition +275%Operating profitJPY 144.0 bnYoY +17.3%post-aquisition +521%Trends in revenue, operating profit, and operating profit margin

- Starting from FY2022 1Q, the business segmentation was changed. Figures from FY2021 onwards are based on the new segmentation and exclude the overseas marine business

- In accordance with IAS 29, hyperinflationary accounting was applied to Turkish subsidiaries starting from FY2022 2Q. Figures from FY2022 onwards reflect the application of hyperinflationary accounting

Non-financial outcomes (2024 results)

-

Human resources/organizations

Human resources/organizations

-

Many initiatives to improve the gender balance

- Ratio of female employees: 24.9%

- Ratio of women in managerial positions: 23.7%

-

Increase of employee engagement

- Employee satisfaction (2024): 76.0%

Brands

Brands

-

Increase the recognition and trust in the NIPPON PAINT brand

- Listed on Brand Finance’s Top 10 Most Valuable Paint Brands in the World for the third consecutive year

Nature/environment

Nature/environment

-

Water usage properly managed based on voluntary standards

- Total water usage: -2.2% YoY

-

Many initiatives to improve the gender balance

-

Customer base

Customer base

-

Comprehensive distribution network to support growth in the

decorative paints business

- Number of stores: c. 260,000

- Number of CCMs: c. 20,000 units

The number of distribution shops in 2024 declined from 2023 due to a detailed review of reporting criteria, such as the exclusion of dormant or non-active shops; If not for the review and under the previous criteria, the total number of distribution shops is estimated to have increased by approximately 5%

-

Strategic partnerships with Chinese real estate developers

- Selected as the No. 1 paint brand by the top 500 Chinese real estate developers for 14 consecutive years

Brands

-

Continuous investment in strengthening the brands’ statuses

- Achieved a 51% Top of Mind score among consumers

Nature/environment

- Introduced comprehensive lifecycle waste management systems to reduce waste, improving recycling efficiency

-

Comprehensive distribution network to support growth in the

decorative paints business

-

Customer base

- Enhanced customer services through the largest number of CCM machines deployed in Indonesia

- Strengthened relationships with fishing communities by providing samples of ship repair coatings

Brands

-

Continuous investments in enhancing brand awareness and positioning

- Achieved a high credible Top of Mind score among consumers for decorative paints

-

External partners

External partners

-

“New Generation Dealer” program and loyalty program

- Number of stores implementing these programs: c. 400

-

Strengthened relationships with dealers and professional painters through the “Filli Ustam” loyalty program

- Number of professional painters using this program: c. 2,600

*The decrease compared to 2023 is due to professional painters relocating outside Türkiye as a result of worsening economic conditions in the country

Brands

-

Strengthened position as the market leader

- Maintained the No.1 position in the decorative paints market for about 20 years

-

“New Generation Dealer” program and loyalty program