Font Size

1. Front Cover - FY2025 4Q Financial Results Presentation Material

Good afternoon, everyone. I am Yuichiro Wakatsuki, Co-President of Nippon Paint Holdings.

Thank you very much for joining us today. I will begin with a review of our fourth-quarter and full-year results for FY2025, followed by an update on our Medium-Term Strategy.

As you know, we typically provide a formal update on our Medium-Term Strategy each April. In 2025, however, we experienced several significant developments, most notably the consolidation of AOC. At our IR Day in November 2025, we discussed these developments in depth, including AOC, NIPSEA China, the Türkiye Group, and our M&A strategy. Given that our overarching strategic direction remains unchanged, today’s update will be streamlined, with a primary focus on recent progress and key developments.

Please also note that members of the press are in attendance today.

2. Supplementary Information

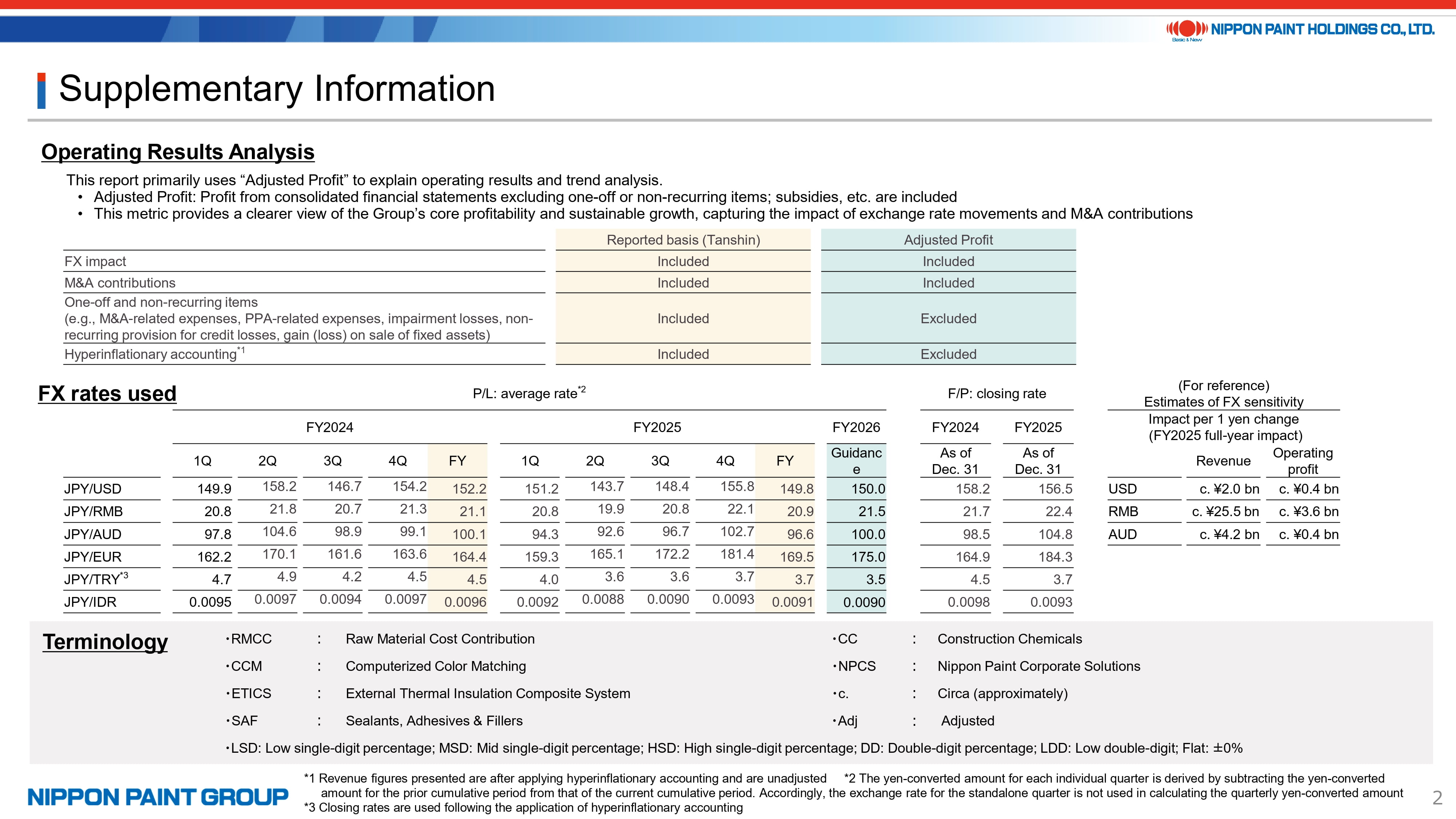

Please note that beginning in the third quarter of 2025, we implemented revisions to our disclosure approach. These enhancements have been generally well received by investors. We remain committed to incorporating constructive feedback from investors and will continue refining our disclosures where appropriate.

We have also updated the way we present foreign exchange information. Rather than disclosing cumulative average rates, we now present the exchange rate for each individual quarter. In the fourth quarter of 2025, the yen was weaker year on year, while on a full-year basis it was slightly stronger. Our assumed FX rates for 2026 are modestly stronger than current spot levels and broadly consistent with the average levels seen in 2025.

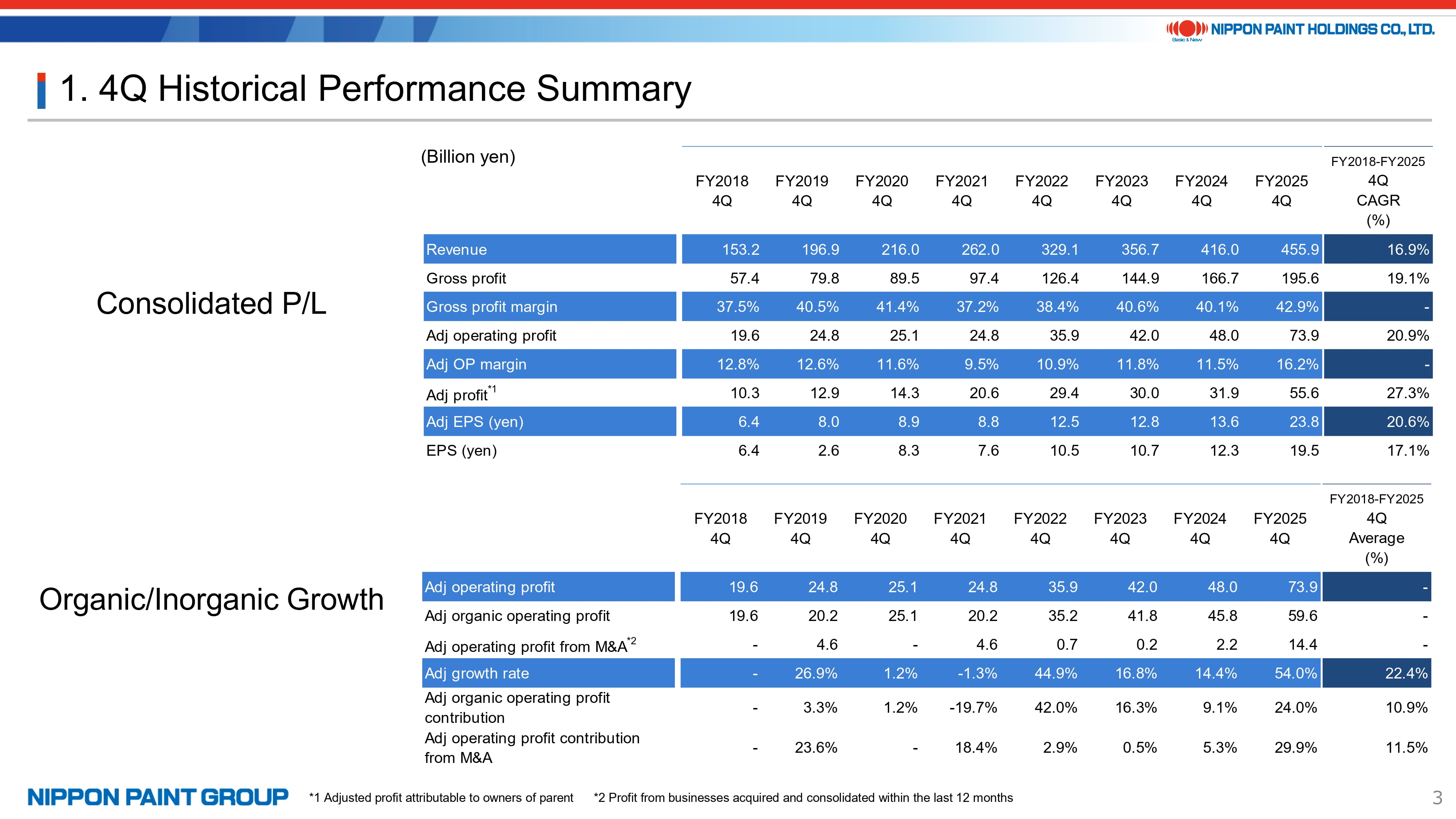

3. 4Q Historical Performance Summary

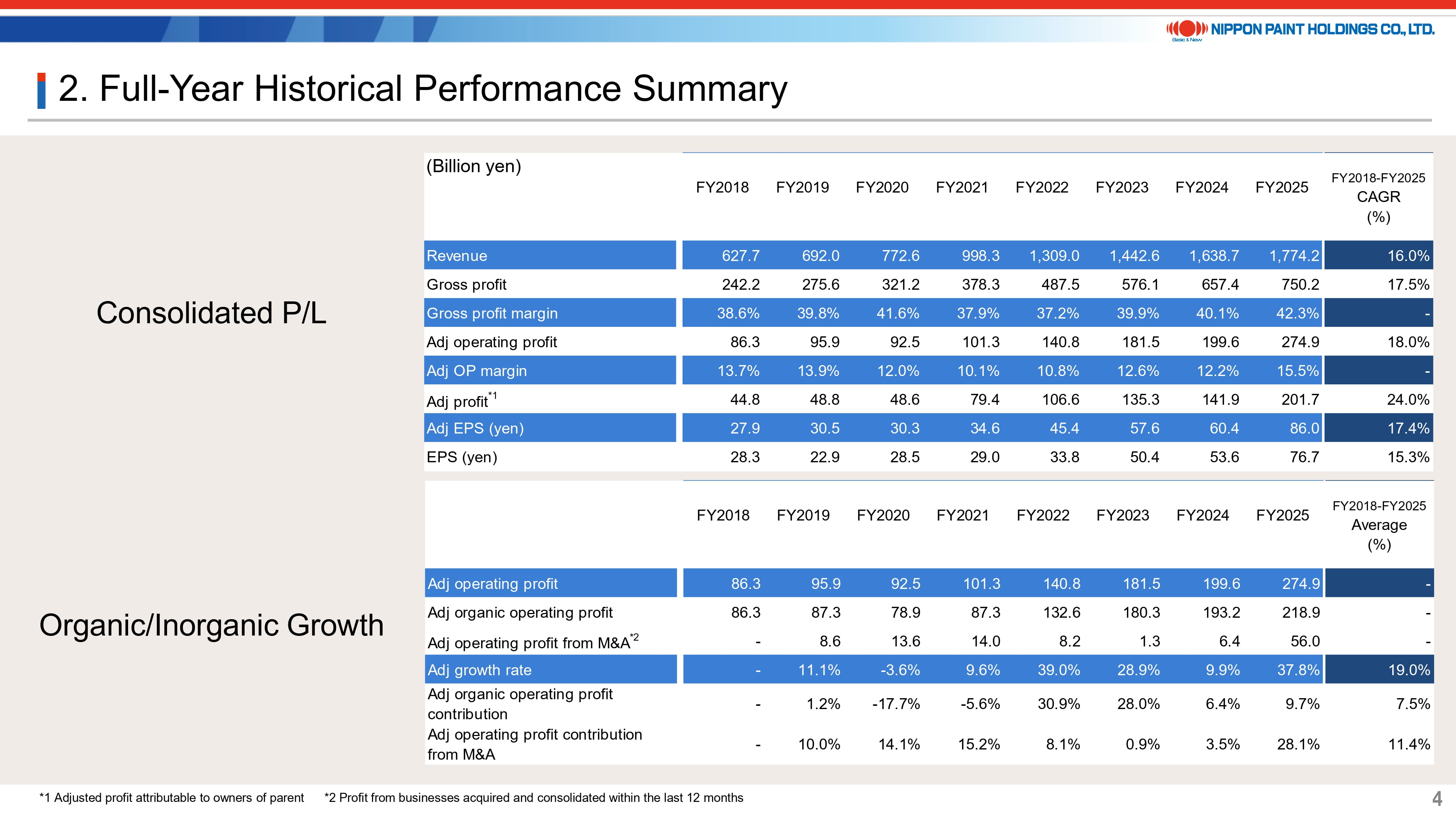

The tables on pages 3 and 4 provide a summary of our long-term performance trajectory. When viewed over time, our fourth-quarter and full-year results underscore our strong and consistent growth track record, supported by both organic and inorganic expansion. and strategic M&A.

Looking specifically at the long-term full-year performance trend, we believe the data highlights the resilience of our organic earnings capacity. Although organic profit growth turned temporarily negative in 2020 due to the impact of COVID-19 and again in 2021 amid a sharp rise in raw material costs, growth has rebounded significantly since 2022.

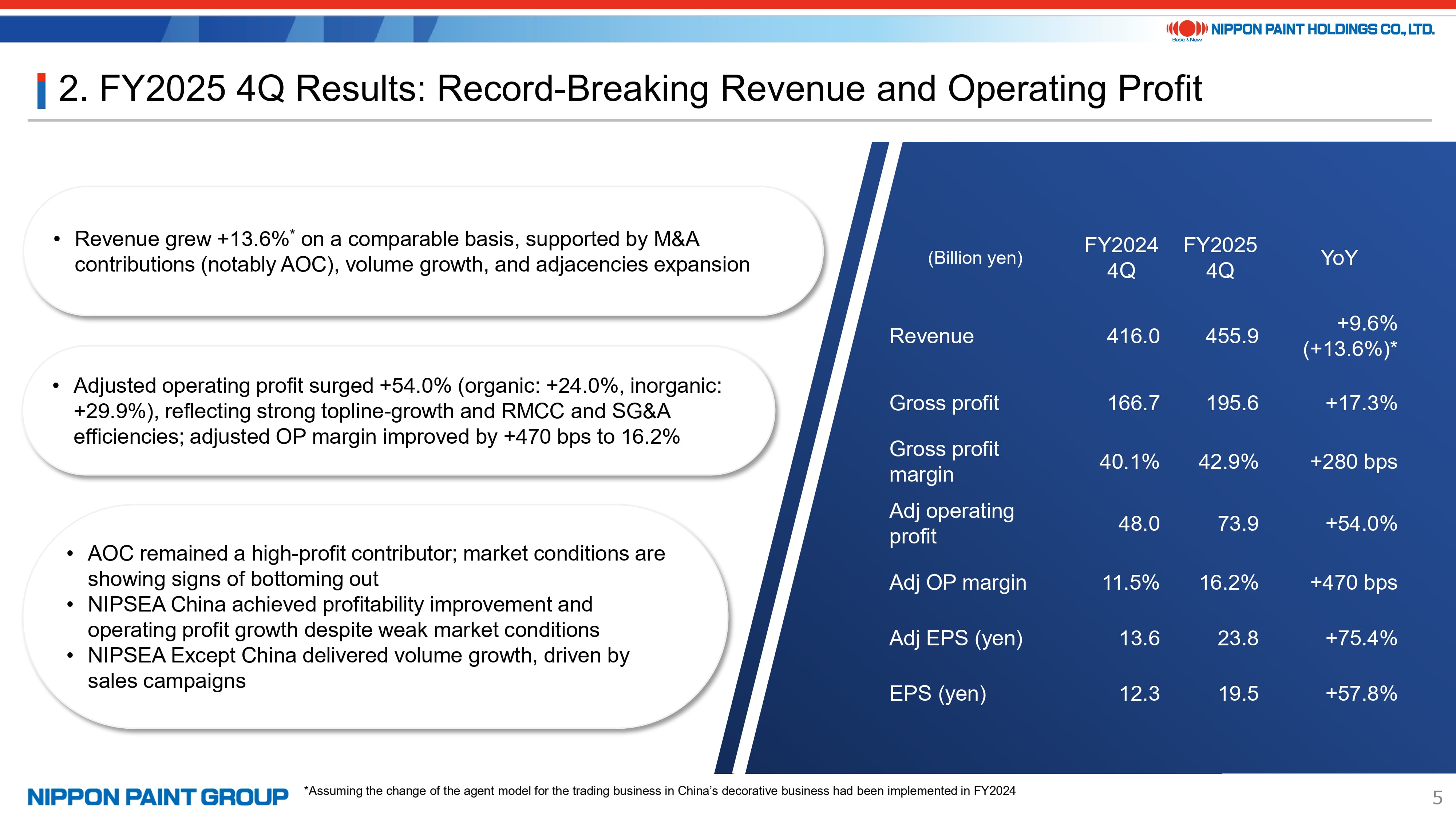

4. FY2025 4Q Results: Record-Breaking Revenue and Operating Profit

Let me now turn to an overview of our fourth-quarter performance for 2025.

We achieved record highs in both revenue and operating profit. Revenue increased by 14%, while adjusted operating profit rose by 54% and adjusted EPS grew by 75%, reflecting a significant expansion in earnings. In terms of the drivers behind adjusted operating profit growth, organic factors contributed 24% and inorganic factors contributed 30%. As a result, our adjusted operating profit margin improved by 470 basis points.

By region, AOC continued to make a strong contribution to overall profitability. Following recent U.S. rate cuts, we are beginning to observe early signs of market stabilization. In NIPSEA China, although macroeconomic conditions remained challenging, we maintained a disciplined, margin-focused approach and continued to deliver profit growth. In NIPSEA Except China, volumes showed broad-based improvement.

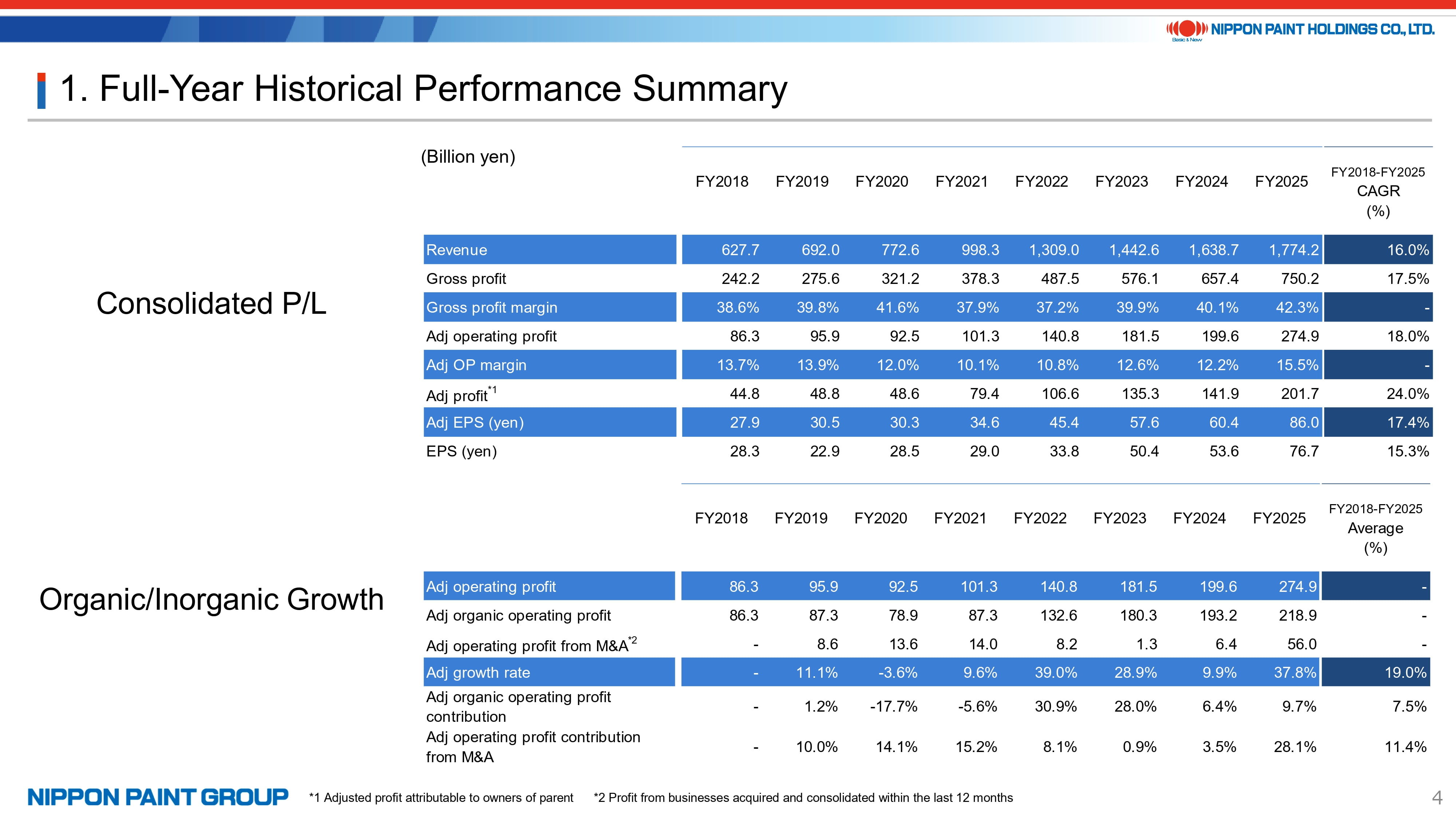

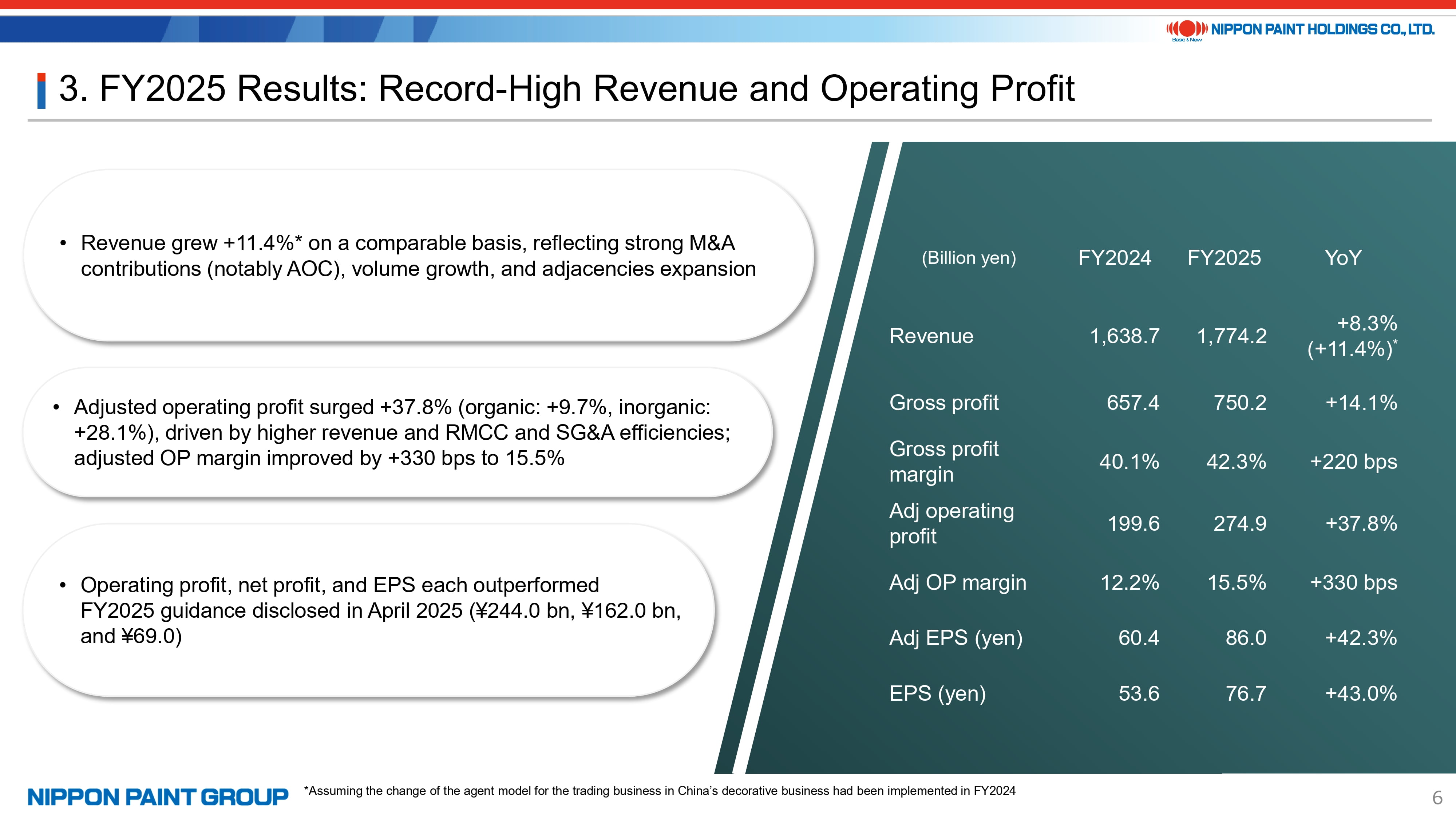

5. FY2025 Results: Record-High Revenue and Operating Profit

Next, I will review our full-year results for 2025.

Revenue increased by 11% year on year, while adjusted operating profit rose by 38%. As a result, our adjusted operating profit margin improved by 330 basis points to 15.5%. Adjusted EPS increased by 42.3%. Reported EPS reached JPY 76.7, and together with operating profit and net profit, we significantly exceeded the guidance announced in April 2025.

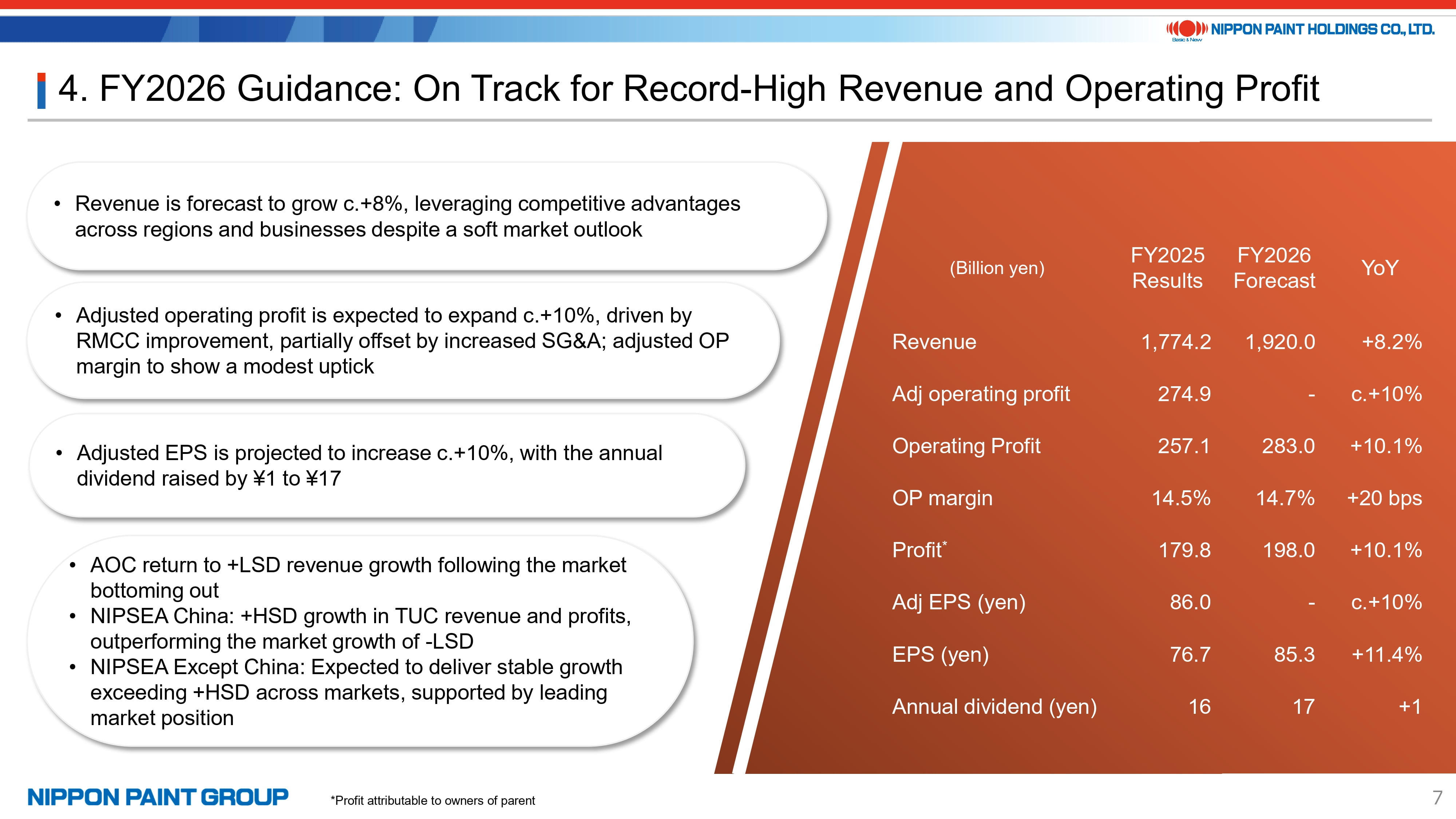

6. FY2026 Guidance: On Track for Record-High Revenue and Operating Profit

Turning to our full-year outlook for 2026, we expect the macroeconomic environment to remain challenging. Nevertheless, we are forecasting new record highs in both revenue and operating profit. We project revenue growth of approximately 8%, with both adjusted operating profit and net profit expected to increase by around 10%. In addition, we anticipate a modest improvement in our adjusted operating profit margin.

Reported EPS is forecast at JPY 85.3, representing an 11.4% increase year on year. This includes slightly more than 100 basis points of uplift attributable to the share buyback program we have been executing since October 2025.

By region, we expect AOC to return to low single-digit revenue growth. In NIPSEA China, as discussed at our IR Day, we anticipate TUC will deliver high single-digit revenue growth alongside continued profit expansion. For NIPSEA Except China, supported by our strong market positions, we expect stable high single-digit - or higher - growth across each market.

With respect to shareholder returns, as announced at the time of the AOC acquisition in October 2024, we have adopted a progressive dividend policy. While we will continue to prioritize deleveraging in order to preserve financial flexibility for future M&A, in light of our solid performance, we are forecasting a JPY 1 increase in the annual dividend.

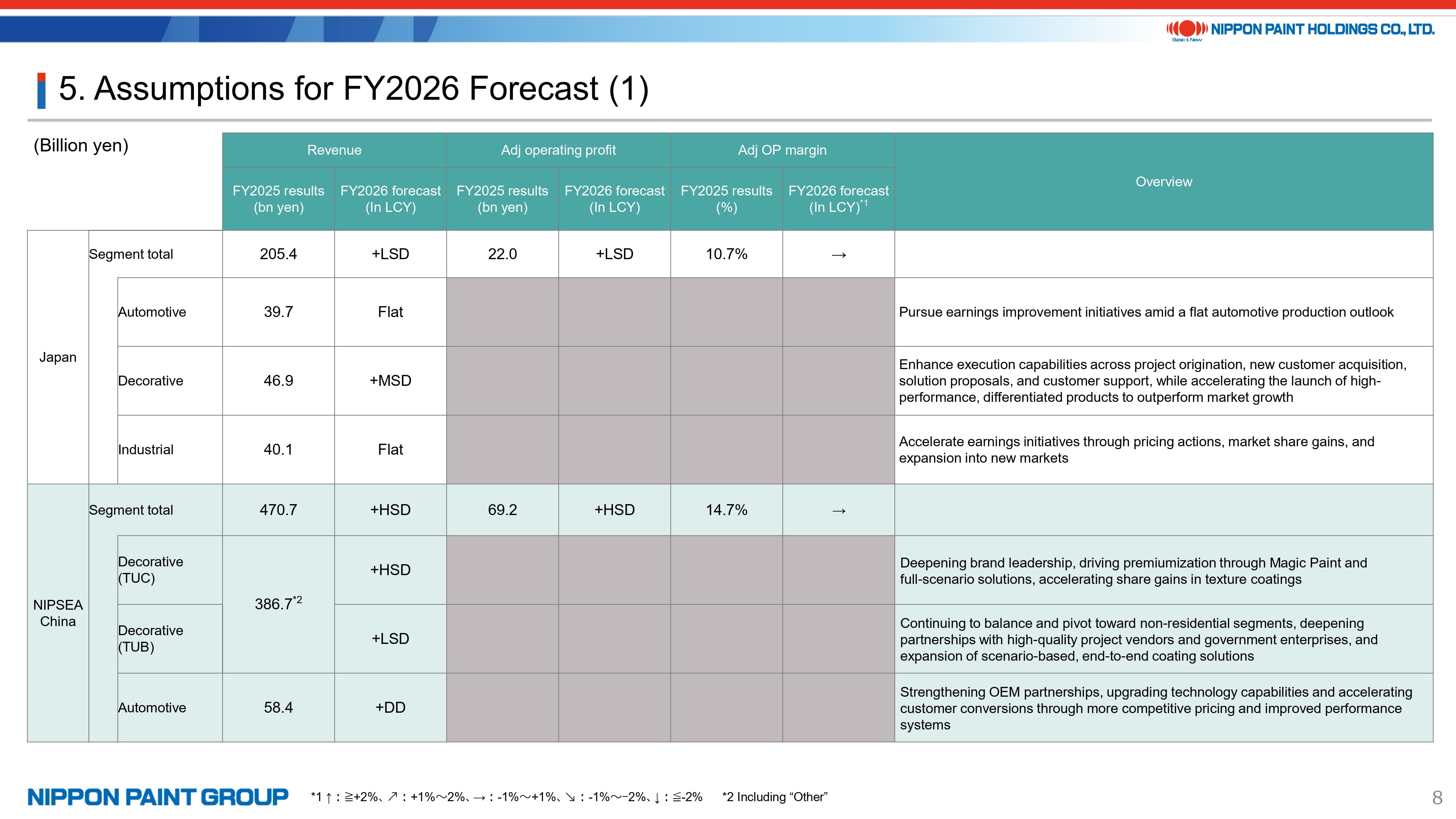

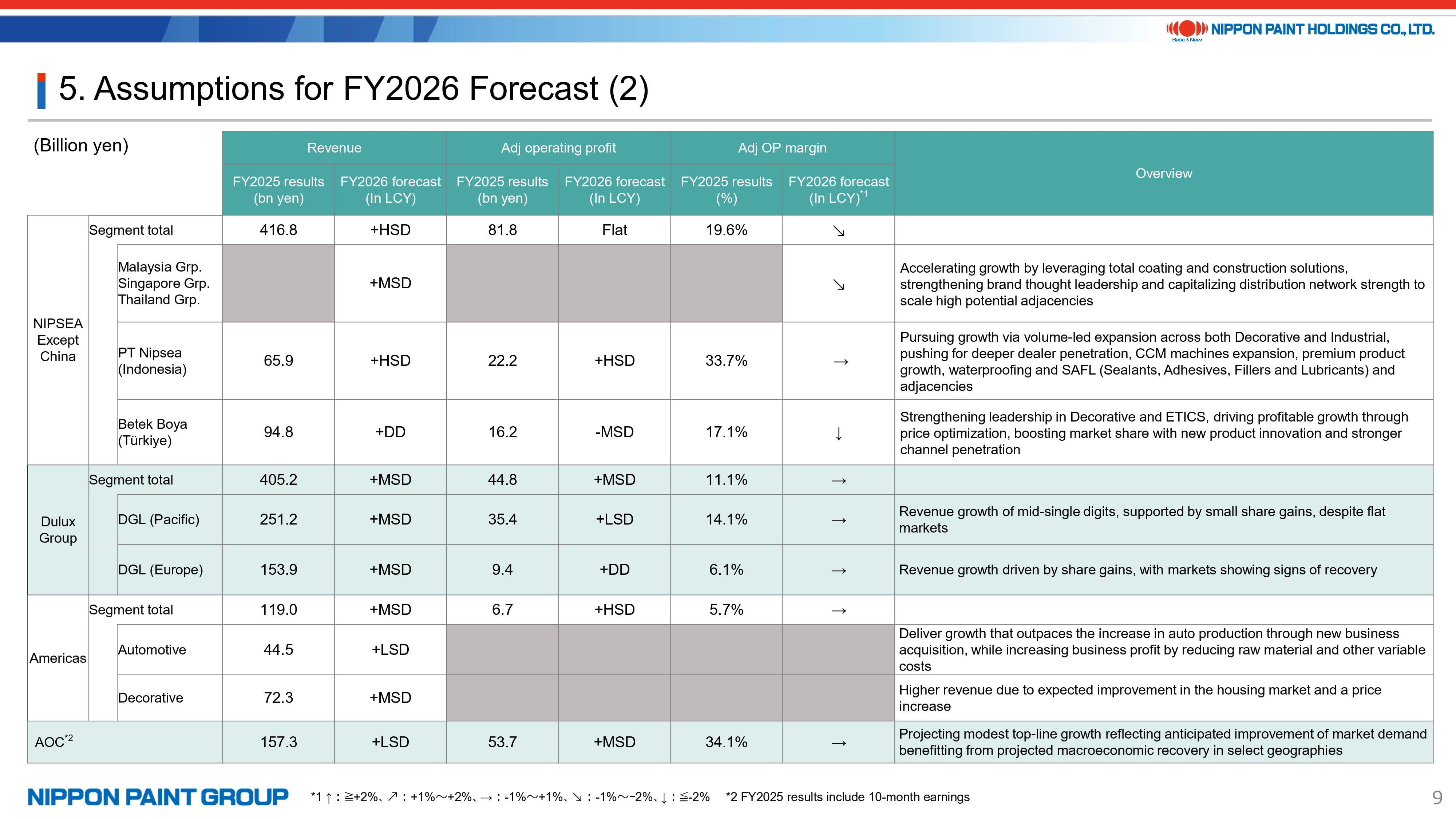

7. Assumptions for FY2026 Forecast

Pages 8 and 9 outline the key assumptions underpinning our segment outlook. In summary, we expect NIPSEA China and NIPSEA Except China to remain the principal engines of revenue growth, while continuing to deliver profitable expansion in each region by leveraging our competitive advantages.

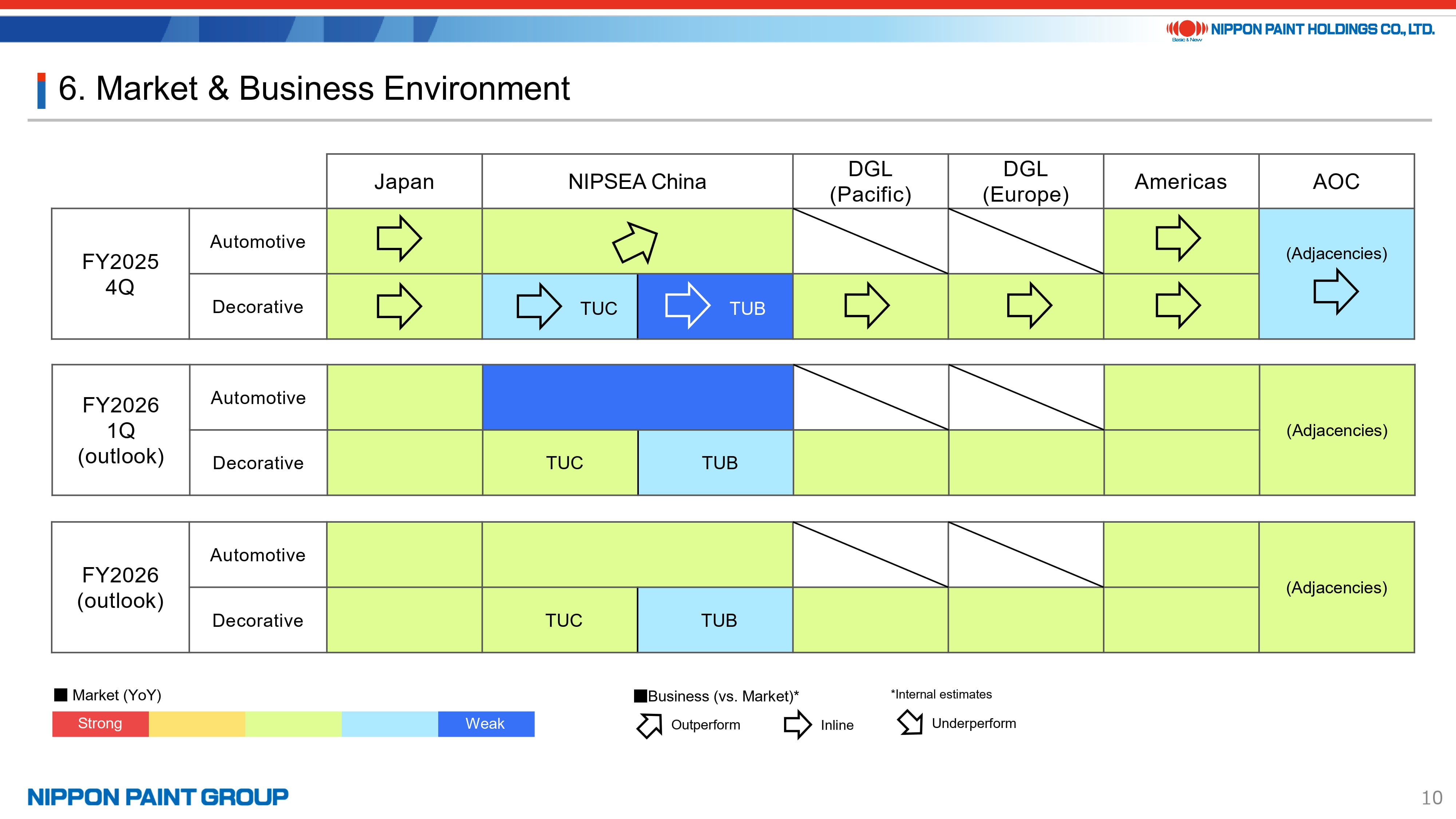

8. Market & Business Environment

Overall market conditions remain challenging, and in this environment, we will maintain a disciplined focus on delivering sustainable and profitable growth.

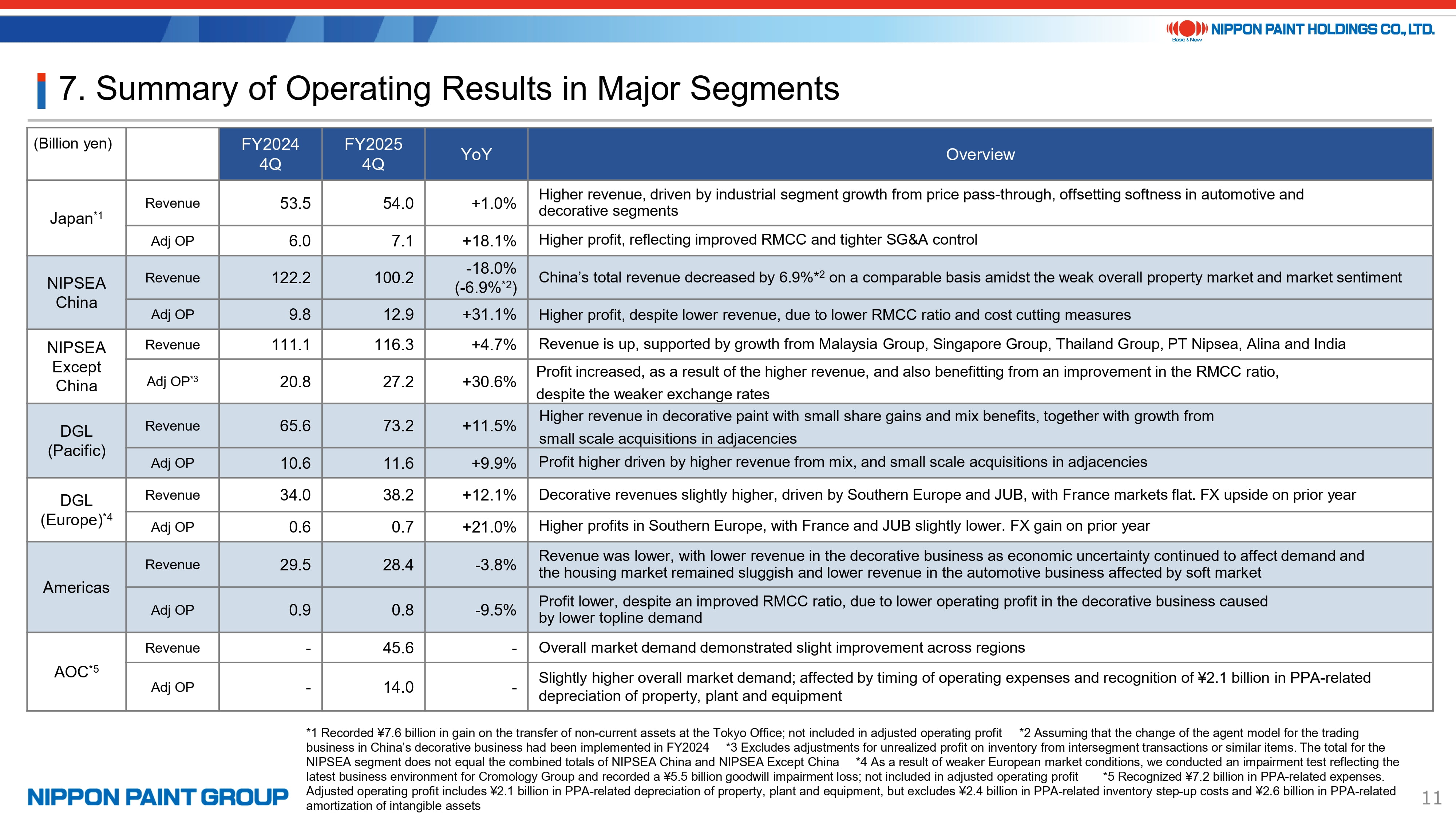

9. Summary of Operating Results in Major Segments

On page 11, I will briefly touch on the performance of our major segments, with further details to be addressed during the Q&A session.

- Japan: Market conditions remained soft, and volumes declined accordingly. However, through an improved product mix, we achieved a slight increase in revenue. Adjusted operating profit rose by approximately 18%, even excluding gains on the sale of non-current assets, supported by an improved raw material cost contribution ratio and disciplined SG&A control. As a result, adjusted operating profit margin improved significantly to 13.1%.

- NIPSEA China: Market conditions were weak across most segments, with the exception of automotive. Nevertheless, we delivered 30% year-on-year operating profit growth in the fourth quarter. Through rigorous cost management, we achieved nearly a 500 basis point improvement in operating profit margin despite softer demand. Looking ahead to 2026, while market conditions are expected to remain challenging, as noted earlier, we aim to return to a revenue growth trajectory by leveraging our competitive strengths.

- NIPSEA Except China: Both revenue and operating profit continued to grow, more than offsetting the negative impact from foreign exchange movements.

- DuluxGroup: In the Pacific region, market conditions were broadly flat. Nevertheless, we delivered near double-digit growth in both revenue and operating profit, supported by volume expansion, an improved product mix, small-scale acquisitions, and favorable FX effects - demonstrating stable and consistent growth. In Europe, market conditions were mixed. France recovered to approximately the prior year’s level, Southern Europe remained strong, while the ETICS (External Thermal Insulation Composite System) market at JUB was weak. Even so, aided by favorable exchange rates, we achieved growth in both revenue and operating profit. However, in light of the deteriorating market environment in Europe, we conducted an impairment test on the Cromology Group and recorded a goodwill impairment loss of JPY 5.5 billion.

- Americas: In the automotive segment, overall automobile production across the Americas declined. In the decorative segment, housing demand softened amid persistently high long-term interest rates. As a result, both revenue and operating profit in the Americas decreased year on year.

- AOC: AOC continued to make a strong profit contribution while maintaining very high margins. For reference, revenue declined by 2% year on year, which we view as an early indication that the market may be approaching a bottom. The PPA process has now been completed. On an unadjusted basis, we recognized a total of JPY 5.1 billion in intangible asset amortization and inventory step-up costs. In addition, JPY 2.1 billion of depreciation on tangible fixed assets is included even in our adjusted figures; excluding this impact, the adjusted operating profit margin would remain at approximately 35%.

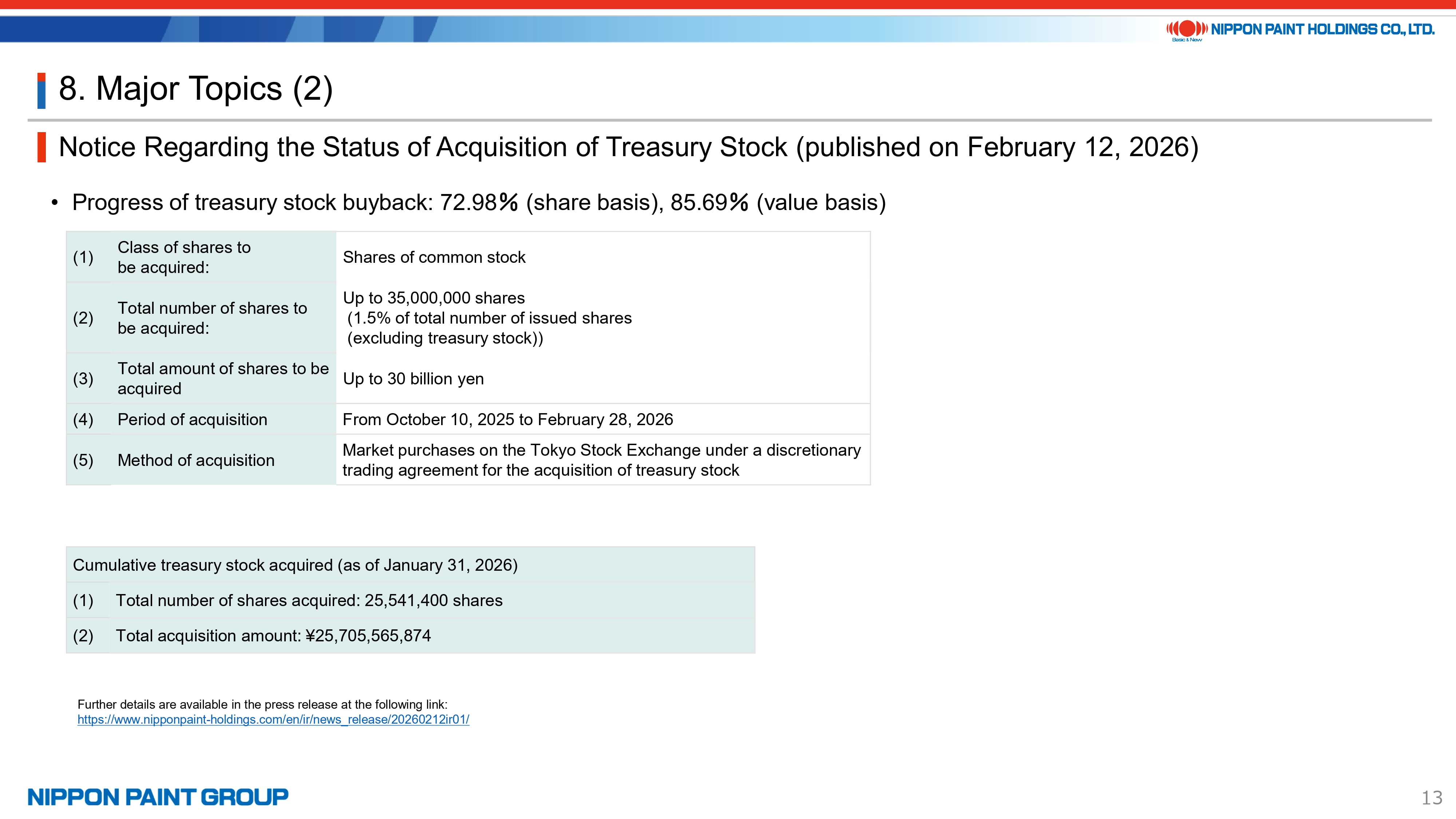

10. Major Topics

There are three key topics to highlight.

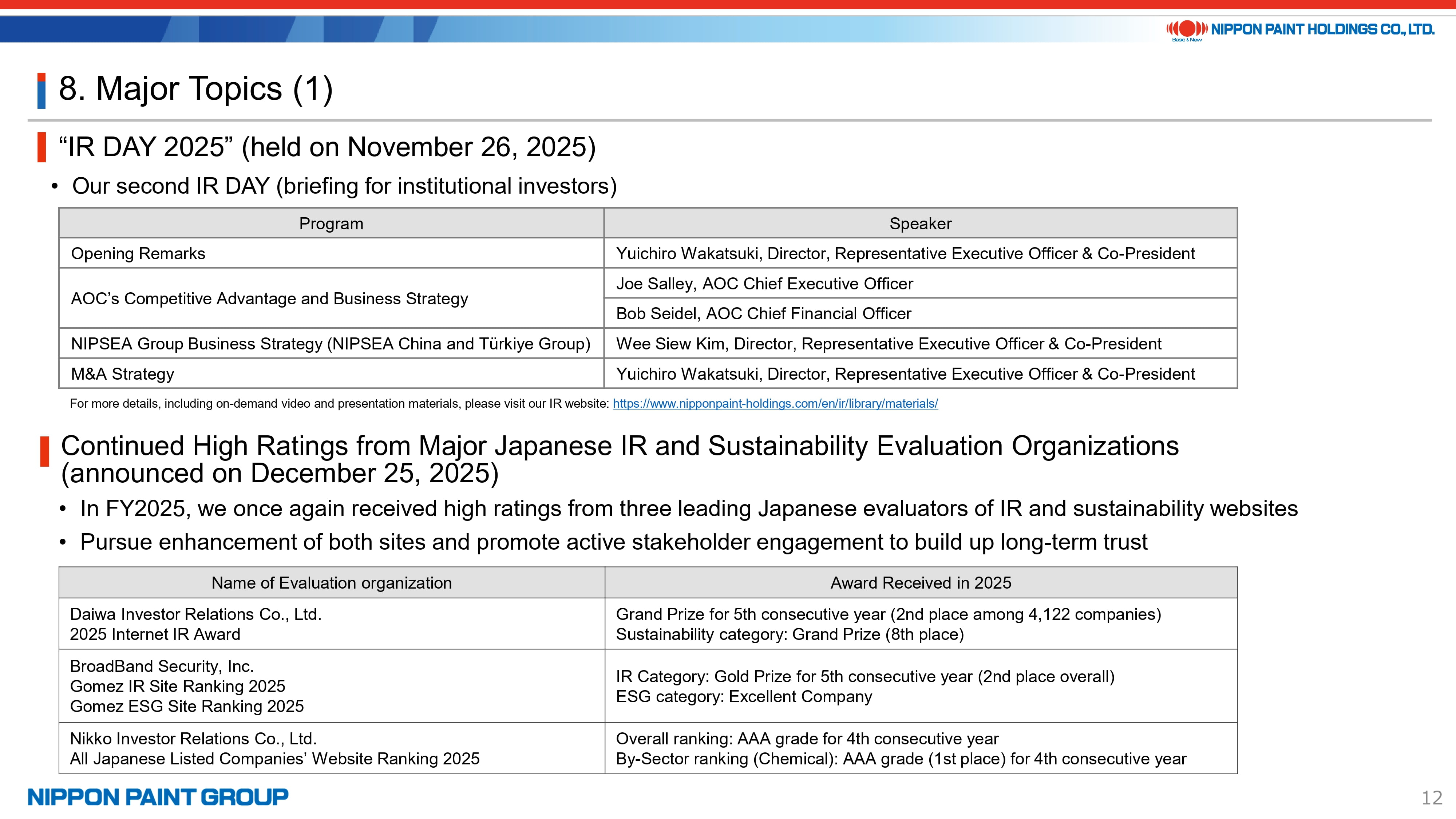

First, as previously announced, we held our IR Day in November 2025.

Second, we continued to receive strong evaluations from external assessors of our IR and sustainability disclosures. We sincerely appreciate the constructive feedback provided, which continues to support the enhancement of our communications.

Third, as announced yesterday, our share buyback program is progressing steadily. While we are naturally disappointed that our share price has been trading at relatively low levels, from a buyback perspective this presents an opportunity to repurchase shares at an attractive valuation. If the program proceeds as planned, we expect it to be largely completed by the end of February, contributing approximately 120 basis points to year-on-year EPS growth.

This concludes the financial results portion of our presentation. I will now move on to provide an update on our Medium-Term Strategy.

11. Front Cover - Nippon Paint Medium-Term Strategy Update Briefing

I will begin with an executive summary.

There have been no fundamental changes to the Medium-Term Strategy originally announced in April 2024 and subsequently updated in April 2025. Accordingly, I will focus my remarks on the key points.

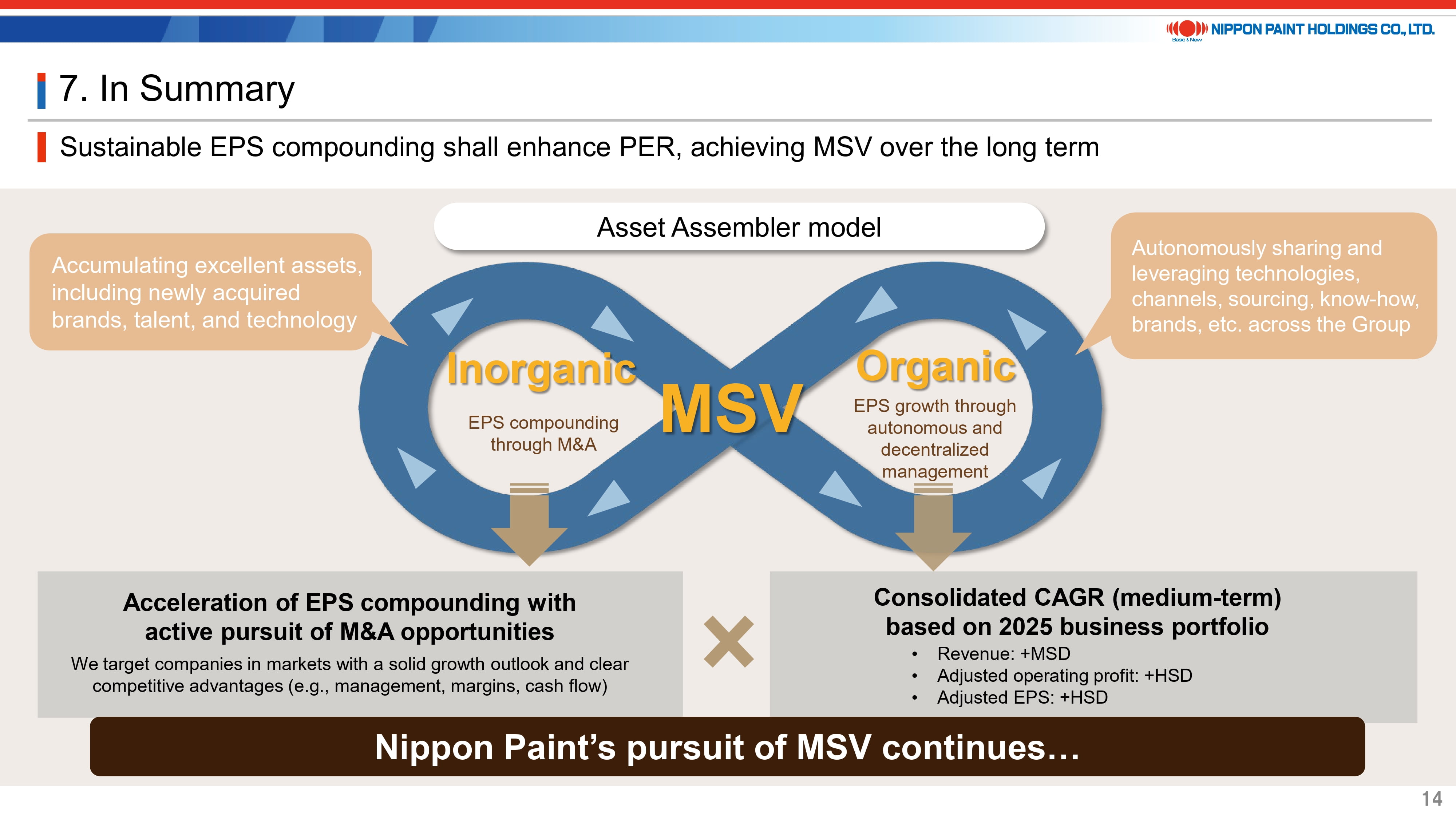

First, we remain firmly committed to our Asset Assembler strategy as the core engine driving unlimited organic and inorganic growth.

Second, our organic growth capabilities remain robust, as demonstrated by our 2025 results despite a challenging market environment. That said, revenue visibility is more limited than it was in 2024. We are therefore adopting a slightly more cautious outlook for growth in NIPSEA China. In addition, with AOC now integrated into our portfolio - operating primarily in the U.S., where near-term market conditions remain somewhat challenging - we expect a degree of short-term dilution to our overall growth rate. As a result, we are modestly revising our medium-term targets from 8–9% revenue growth and 10 - 12% EPS growth to mid single-digit revenue growth and high single-digit EPS growth.

Third, with respect to inorganic growth, we will continue to pursue both bolt-on acquisitions and asset-assembly transactions. Even following the acquisition of AOC, we have remained actively engaged in evaluating new M&A opportunities. While we have walked away from transactions where valuation expectations could not be aligned or where we had concerns regarding long-term business sustainability, we believe the current environment presents a number of attractive opportunities for disciplined buyers. In the past, we have described our M&A scope as having “no limitations.” However, based on investor feedback that this message was overly broad and may not resonate clearly with new investors, we have sharpened our focus. Going forward, we will prioritize opportunities within the chemicals domain, targeting businesses operating in resilient growth markets with clear competitive advantages and strong potential to accelerate under our Group platform. We will pursue transactions that are EPS-accretive from year one and capable of achieving ROIC above WACC within approximately three years. To reiterate, M&A is not an objective in itself. We will continue to approach opportunities with strict discipline, including with respect to valuation.

12. Full-Year Historical Performance Summary

This slide is carried forward from our FY2025 fourth-quarter results presentation. From 2018 to 2025, we achieved a revenue CAGR of 16% and an adjusted EPS CAGR of 17.4%. Please note that the EPS growth shown here is calculated after adjusting for the impact of the equity issuance in 2021, which was undertaken in connection with the full integration of our Asian joint ventures and the acquisition of the Indonesia business. We believe these figures clearly demonstrate our long-term growth capability through a balanced combination of organic and inorganic expansion, and we remain committed to consistently delivering on our commitments.

13. Review of Our Medium-Term Strategy (Launched in April 2024)

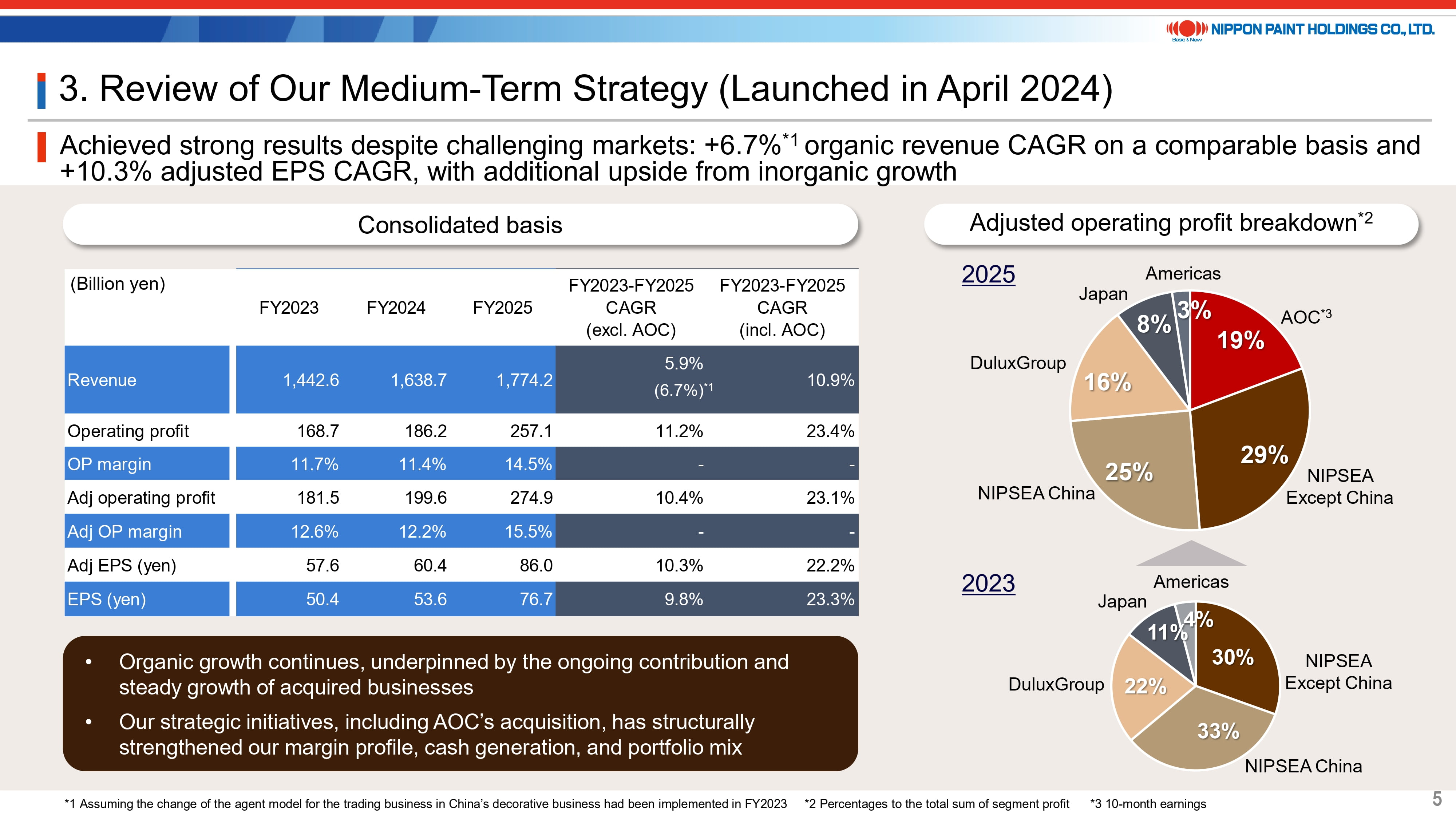

This page provides a brief review of developments since we first disclosed our Medium-Term Strategy in April 2024.

At that time, we did not anticipate the acquisition of AOC and communicated medium-term targets of 8–9% revenue growth and 10–12% EPS growth. Over the past two years, on an organic basis, we delivered just under 7% revenue growth and slightly above 10% adjusted EPS growth - broadly in line with those targets. Considering the significant political and economic changes since April 2024, we believe this represents a strong performance. With the addition of AOC, we achieved 11% revenue growth and 22.2% growth in adjusted EPS. Revenue growth would have been approximately 12% assuming the change in the agent model for China’s decorative trading business had been implemented in 2023. Compared with 2023, our margins and cash generation have improved, and our overall business portfolio has become more balanced.

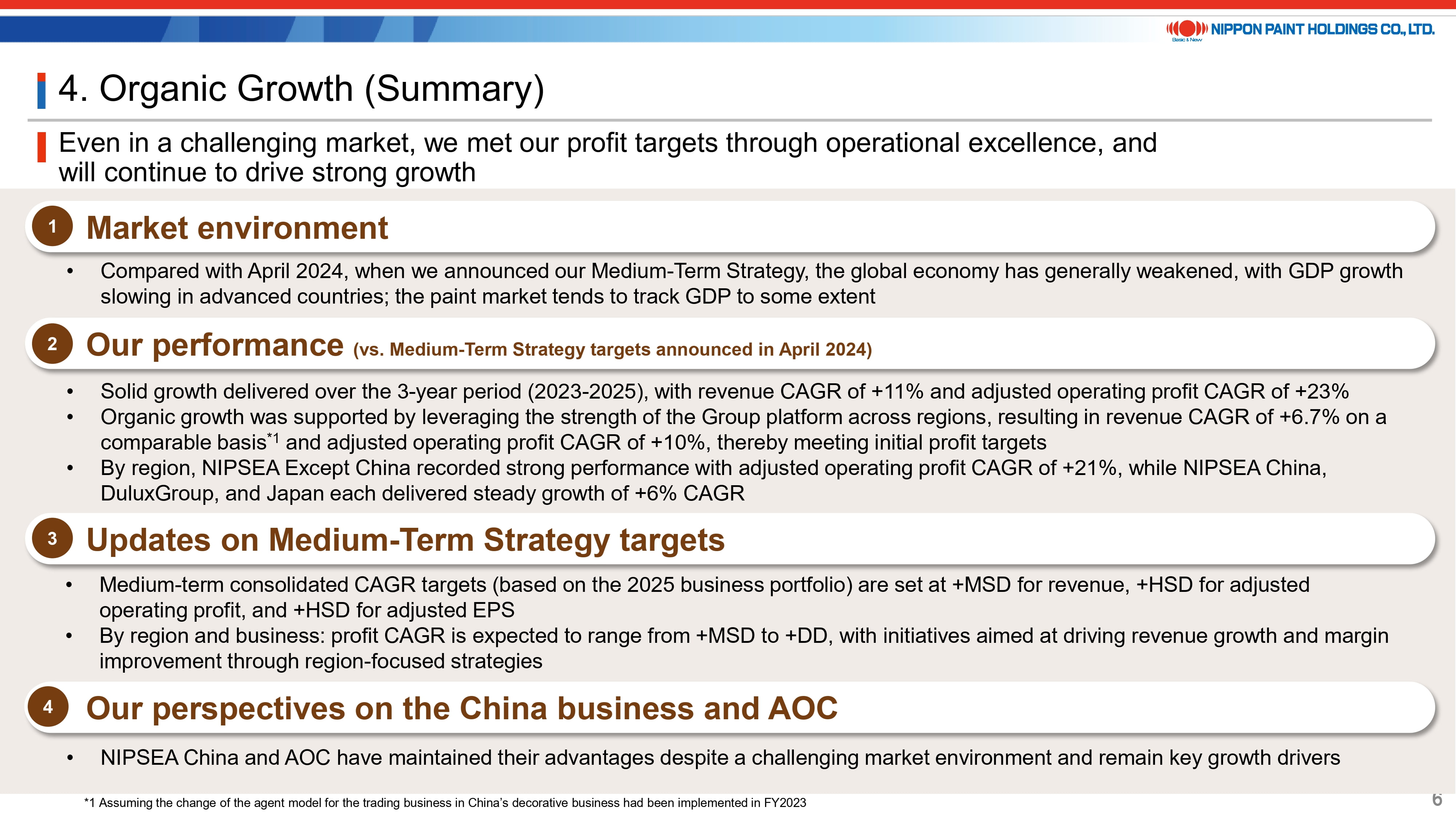

14. Organic Growth (Summary)

Next, let me provide a summary of our organic growth outlook.

As we have consistently emphasized, the paint and coatings industry - particularly decorative paints - benefits from structurally resilient demand. Over the long term, demand expands steadily, supported by population growth, urbanization, and rising living standards. At the same time, it remains influenced by broader macroeconomic conditions. In light of the current environment, we believe it is prudent to adopt a measured and appropriately cautious set of assumptions.

Against this backdrop, as mentioned earlier, we delivered very strong organic growth, even excluding the consolidation impact of AOC. This continued organic expansion and solid cash generation provide a robust foundation from which we can pursue further growth.

With respect to our medium-term targets, based on our current portfolio, we are aiming for mid single-digit revenue growth and high single-digit growth in adjusted EPS. That said, internally, we remain focused on achieving double-digit growth.

Finally, as we emphasized at IR Day, both our China business and AOC continue to represent compelling growth platforms, and our conviction in their long-term potential remains unchanged.

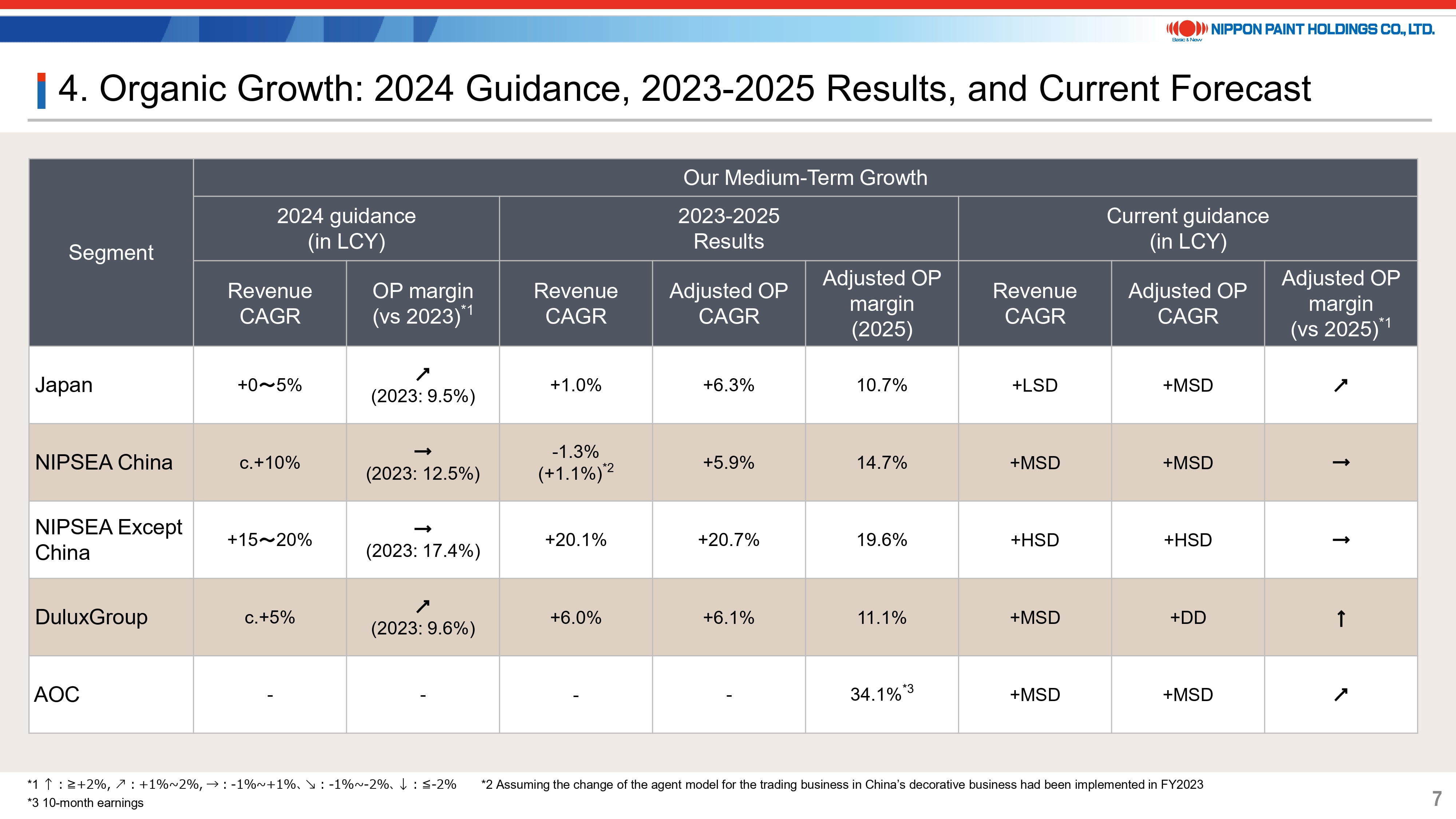

15. Organic Growth: 2024 Guidance, 2023-2025 Results, and Current Forecast

This page compares our actual results for 2023–2025 with the assumptions we outlined in 2024, along with the outlook discussed earlier.

Japan: Operating margin improved broadly in line with our guidance, rising from 9.5% in 2023 to 10.7% in 2025 on an adjusted basis.

NIPSEA China: As mentioned, market conditions remained challenging, and our margin-first approach is clearly reflected in the results. Adjusted operating profit CAGR was 5.9%, somewhat below our original expectations. However, this shortfall was more than offset by the strong performance of NIPSEA Except China.

DuluxGroup: Performance has been broadly in line with our guidance. Looking ahead, a key factor will be the extent to which the recovery in Europe - particularly in France - continues.

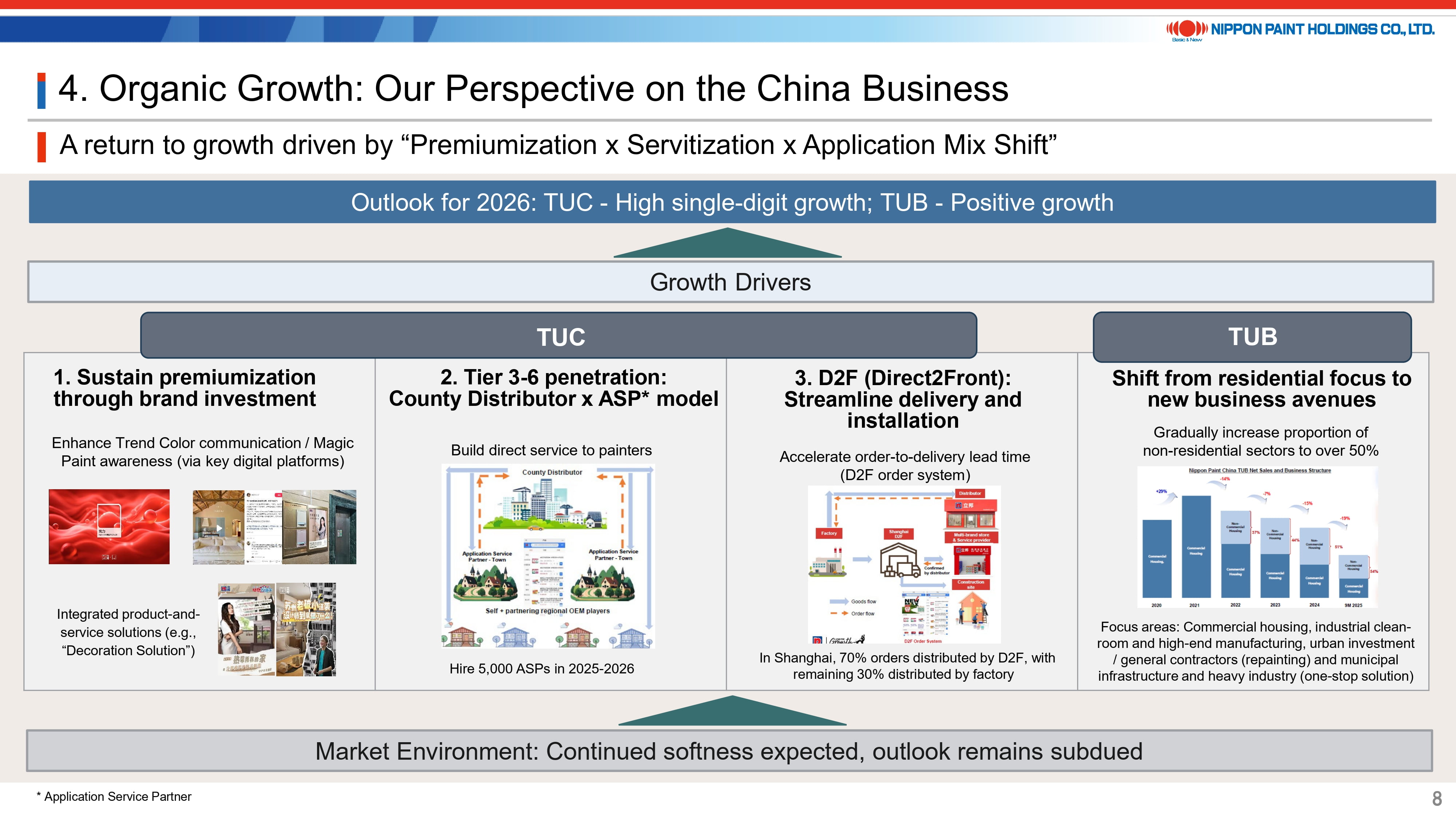

16. Organic Growth: Our Perspective on the China Business

With respect to NIPSEA China, Wee Siew Kim provided a detailed update at IR Day, so I will not repeat those points here. In summary, we are assuming that market conditions will remain soft; however, we intend to pursue growth more proactively. For 2026, we are targeting high single-digit revenue growth for TUC. That said, as shown on the previous page, for NIPSEA China overall, we consider mid single-digit revenue growth to be a realistic medium-term assumption. At the same time, we will continue refining our local initiatives with the aim of outperforming that level.

As we have consistently stated, China is an exceptionally dynamic market. We believe we are uniquely positioned, supported by strong brands, scale advantages, IT-driven capabilities, and our ability to develop new operating models across Tier 3 to Tier 6 cities. Should the market recover - something we are not currently factoring into our assumptions - we believe we will be among the best positioned to capture the upside.

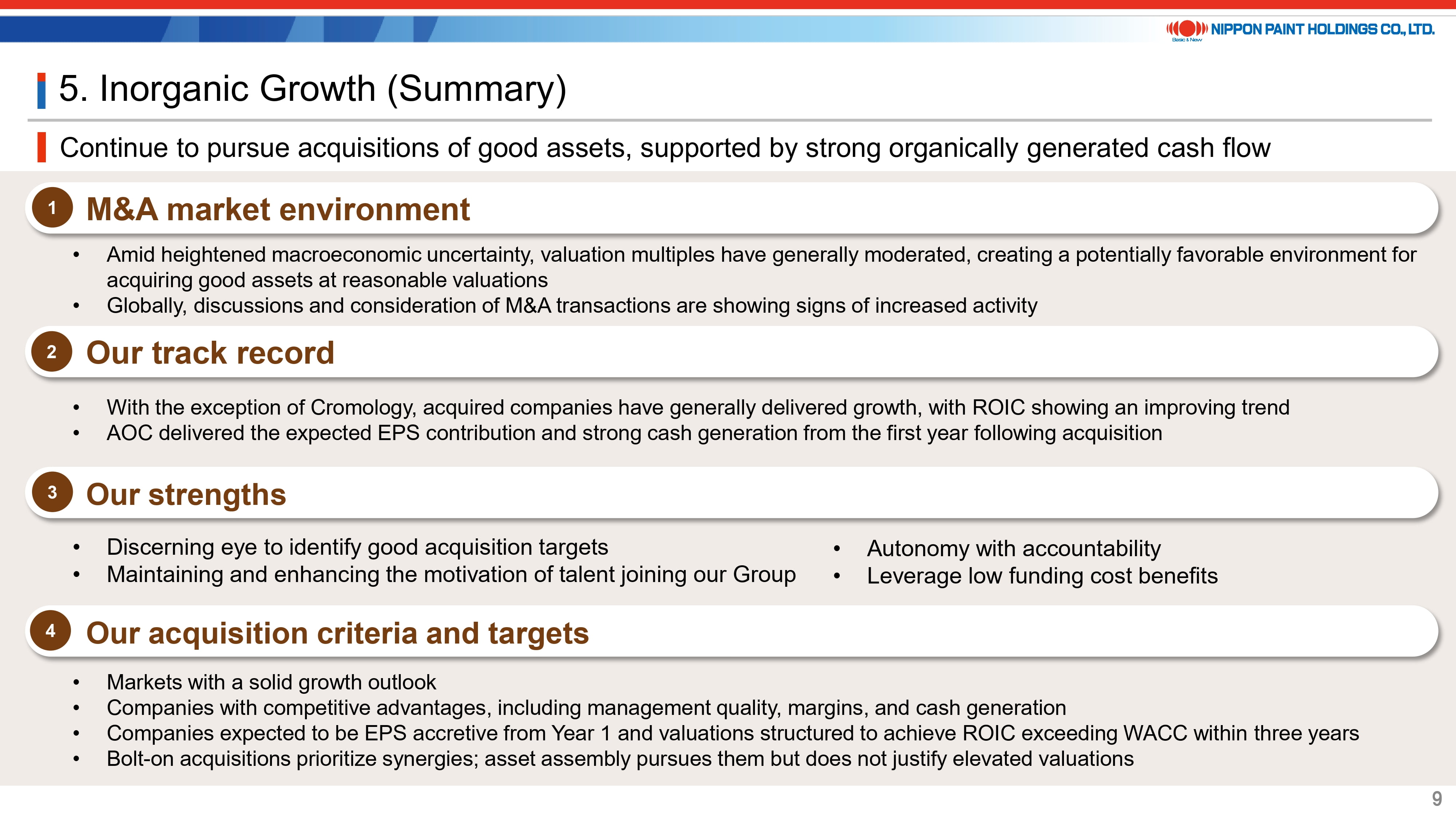

17. Inorganic Growth (Summary)

Next, let me turn to inorganic growth and M&A.

From a market perspective, amid ongoing macroeconomic uncertainty and a broad reset in valuation multiples, we believe the current M&A environment presents attractive opportunities for disciplined buyers. In fact, we are seeing deal-related discussions becoming increasingly active.

At the same time, our track record remains solid. AOC has already made a meaningful contribution, and as I will demonstrate on the following pages, the businesses we have acquired over the years have continued to grow and steadily enhance their returns.

Our advantage in accessing low-cost funding remains intact. That said, as interest rates have risen, our sensitivity to risk has naturally increased, leading us to take a more cautious stance. Even under current funding conditions, however, we believe there remain ample acquisition opportunities that can be pursued without compromising our financial soundness.

Our acquisition criteria and target profile are as outlined earlier. I would also like to address a point raised in investor feedback: we are by no means disregarding ROIC. On the contrary, as our valuation has moderated, our focus on ROIC has become even more disciplined, and we have correspondingly tightened our acquisition standards. At the same time, we do not intend to become overly ROIC-centric in a way that constrains our growth ambition. We believe the appropriate course is to maintain a well-balanced approach between financial discipline and long-term value creation.

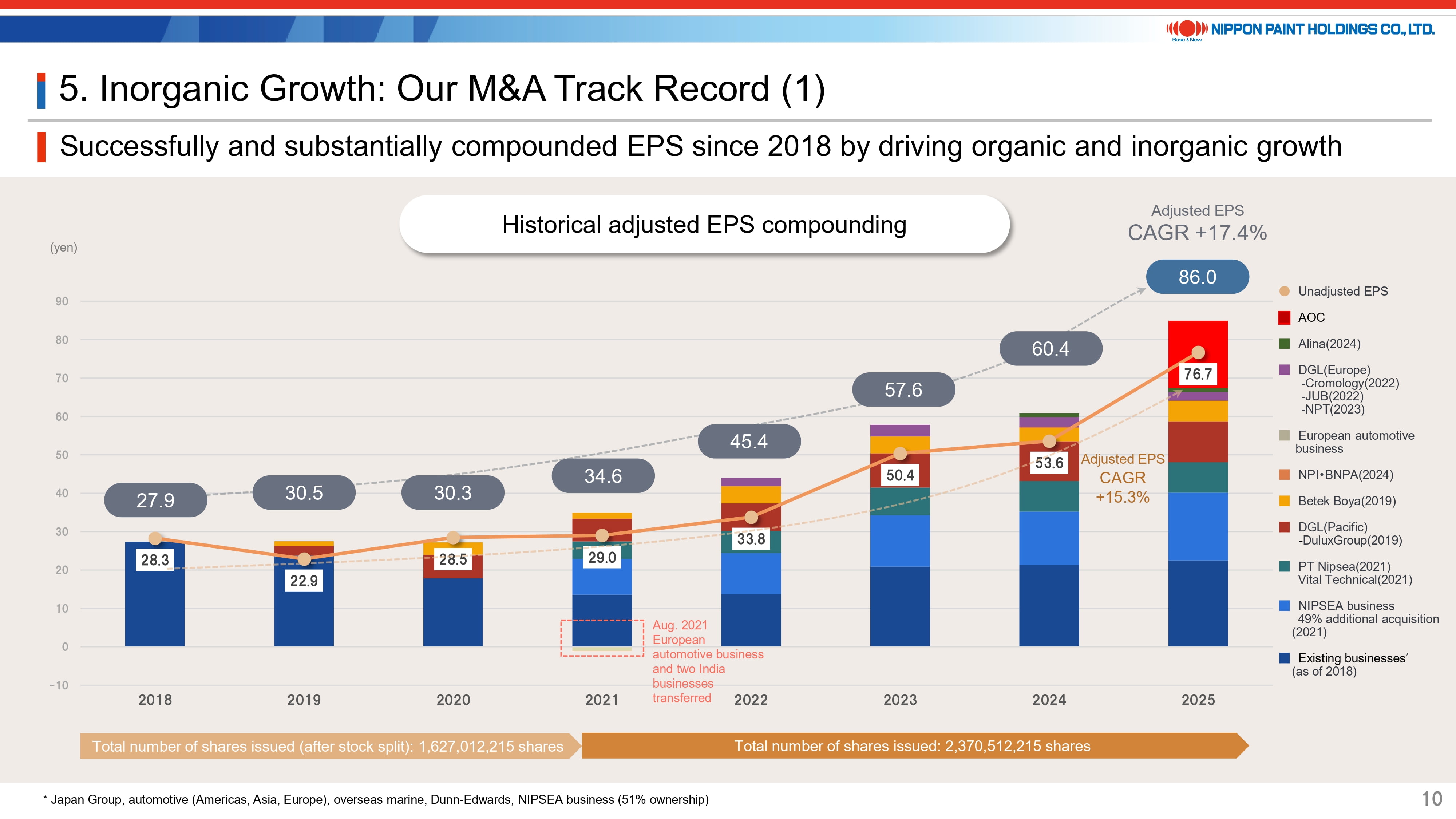

18. Inorganic Growth: Our M&A Track Record (1)

This page presents an updated overview of our EPS compounding track record, which we have highlighted on several occasions.

To ensure there is no misunderstanding, let me clarify this point once again. In 2021, our share count increased by 46% following the full integration of our Asian joint ventures and the acquisition of the Indonesia business. As a result, the EPS contribution from our existing businesses may have appeared to decline temporarily due to the higher share base. However, on a total basis, EPS increased, as the earnings contribution from the newly integrated businesses more than compensated for the dilution effect.

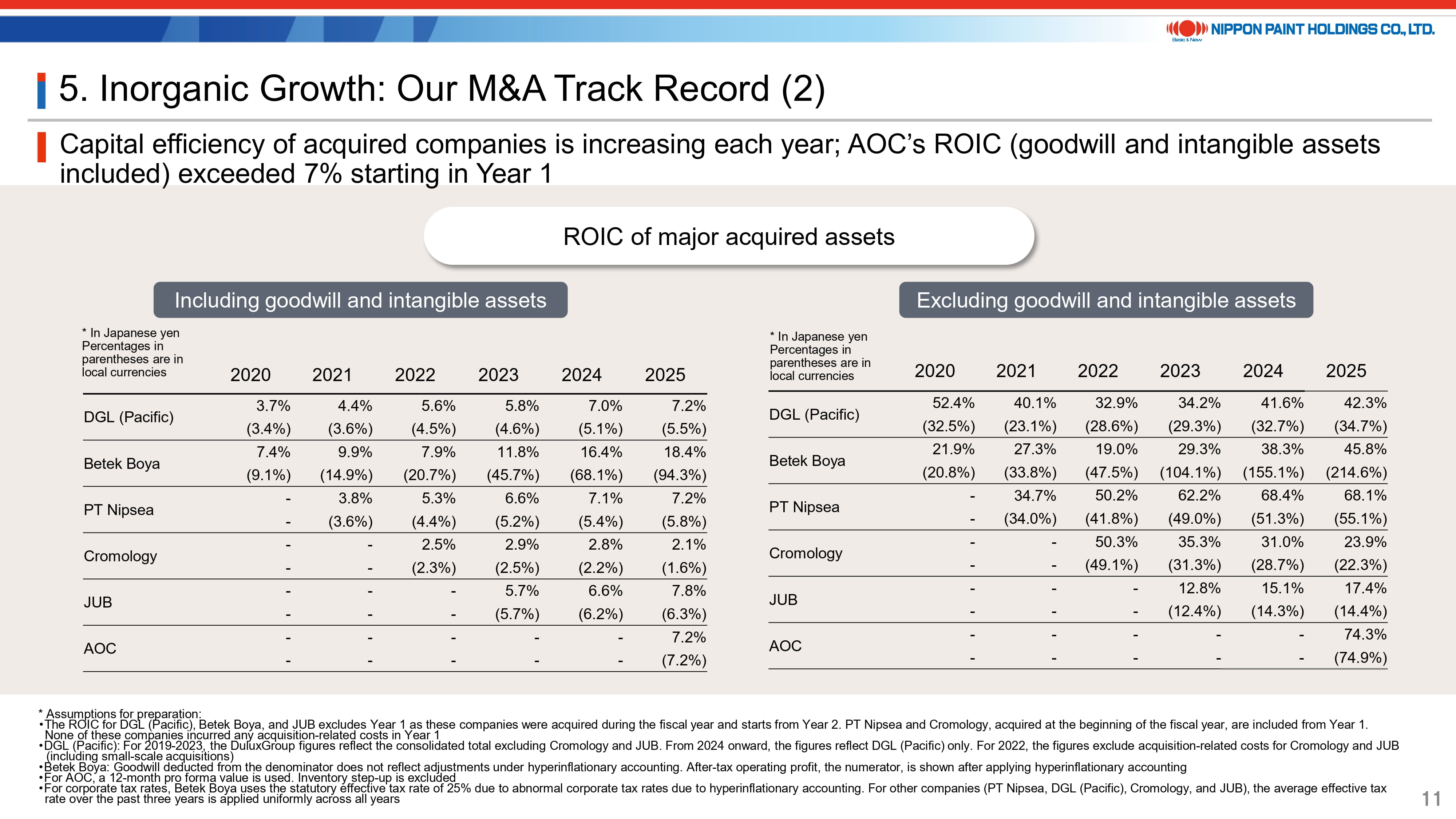

19. Inorganic Growth: Our M&A Track Record (2)

This page provides an updated overview of ROIC trends by asset, which we also presented at our IR Day. We disclose ROIC on two bases: including goodwill and intangible assets, and excluding them. Please keep the following three points in mind:

- ROIC for each asset has improved steadily since acquisition. This reflects not only our disciplined approach to identifying high-quality targets, but also the effectiveness of our management model, which emphasizes autonomy and accountability. In addition, synergies are being realized in practice - both tangible and intangible - further supporting performance improvement.

- The purchase consideration we pay in acquisitions includes goodwill and intangible assets, and therefore these elements cannot be disregarded. That said, we believe the data clearly demonstrates that our acquisitions have consistently focused on asset-light, high-return businesses.

- We are sometimes compared with peers based solely on a company-wide ROIC benchmark. However, companies that actively pursue M&A and those that do not typically have fundamentally different asset compositions and growth profiles. While some investors attempt to adjust for these differences, we believe that an overly ROIC-centric evaluation, as mentioned earlier, can overlook the distinctive strengths and value-creation model that set us apart.

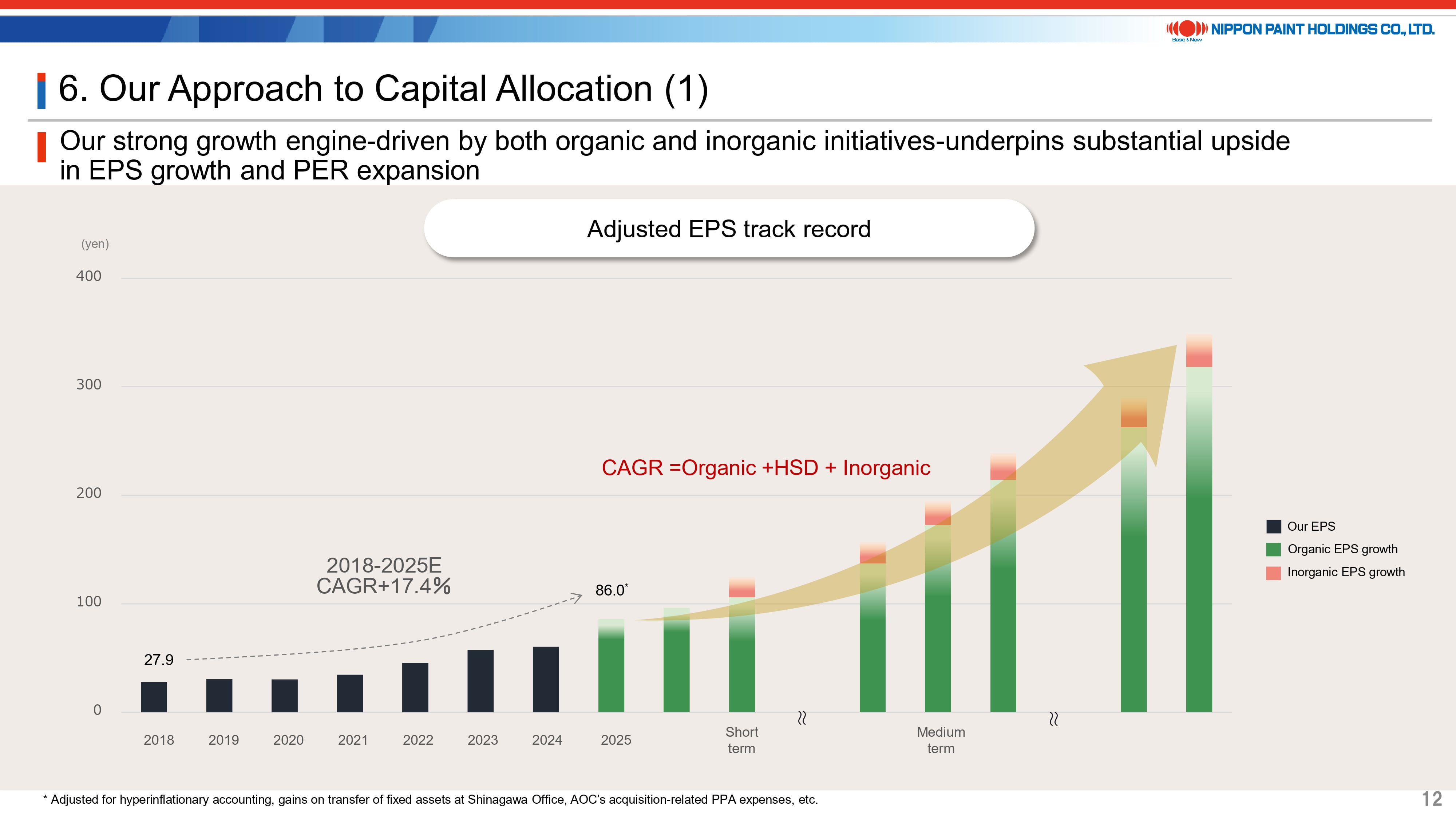

20. Our Approach to Capital Allocation (1)

This slide revisits a key message from our IR Day. The significant capital generated through organic EPS growth will be reinvested into M&A that advances our goal of Maximization of Shareholder Value (MSV), thereby enabling us to sustain strong growth.

What is essential is that investors recognize the credibility and repeatability of this growth model- both organically and inorganically. We remain committed to further strengthening our track record in the years ahead.

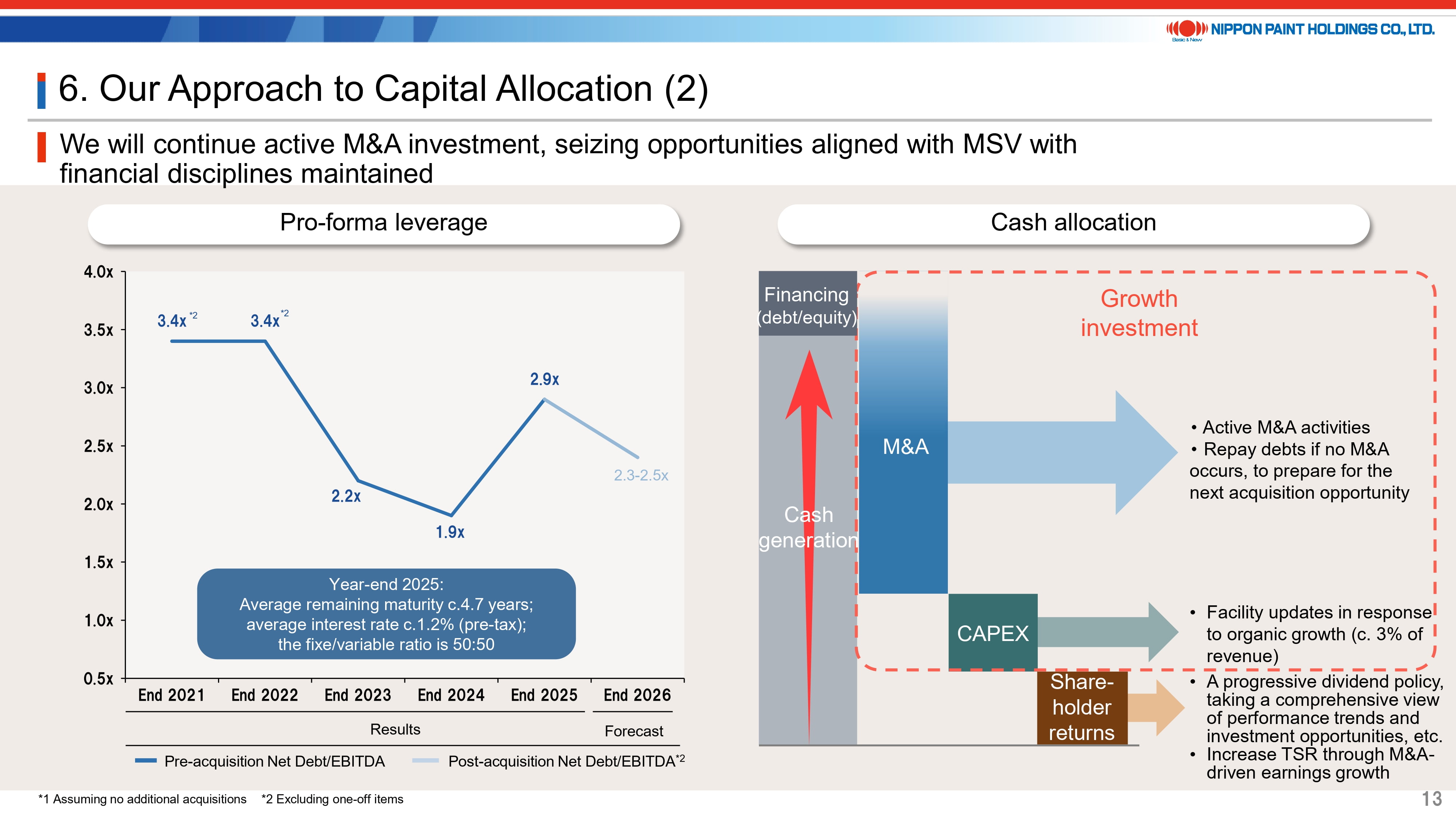

21. Our Approach to Capital Allocation (2)

Our financial discipline remains firmly intact. We will continue to pursue growth while maintaining prudent financial management, guided by a net debt-to-EBITDA ratio of no more than 4.0x and a D/E ratio of no more than 1.0x. As of the end of 2025, our net debt-to-EBITDA stood at 2.9x, even after executing a meaningful level of share buybacks - an outcome that exceeded our expectations. Based on our current projections, we anticipate leverage will decline by approximately 0.5x in 2026. As noted at IR Day and reiterated today, we continue to actively evaluate potential M&A opportunities, and we believe our current financial position provides ample capacity to proceed when appropriate.

22. In Summary

Finally, our commitment to MSV remains unwavering. We believe that few companies express MSV as clearly and unequivocally as their core mission. More importantly, MSV is deeply embedded throughout our organization, guiding our decision-making and execution. We remain fully committed to delivering sustainable results in line with that principle.

Thank you for your attention.