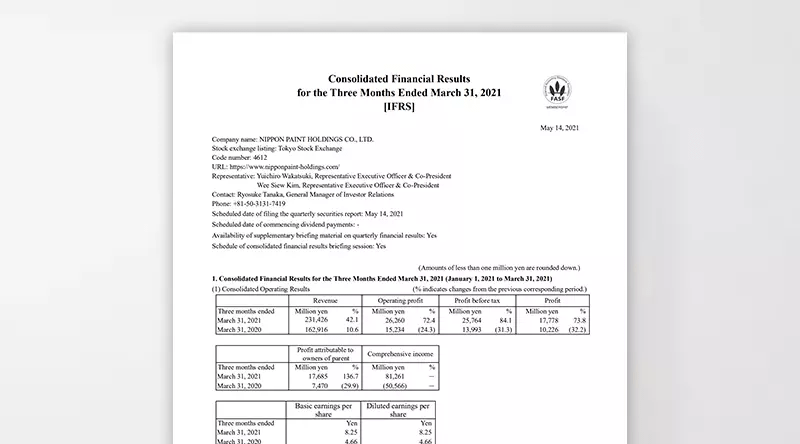

Earnings Forecast (FY2026 Outlook)

For the fiscal year ending December 31, 2026, the decorative paints market and the global automotive market are expected to remain generally stable.

Under these conditions, the Nippon Paint Group will continue to leverage its Asset Assembler model to pursue sustainable growth, with a focus on steadily compounding EPS through the growth of existing businesses and active pursuit of M&A opportunities. The Group aims to expand distribution channels and enhance brand equity across all regions and businesses, drive continued growth in the paint and coatings business through new product development, and reinforce the adjacencies business, including ETICS (External Thermal Insulation Composite Systems), CASE* and colorants. In addition, by promoting autonomous management at Group partner companies worldwide, the Group seeks to expand market share across all regions and business domains.

Based on this outlook, consolidated revenue is expected to be ¥1,920 billion, operating profit ¥283 billion, profit before tax ¥274 billion, and profit attributable to owners of the parent ¥198 billion for the fiscal year ending December 31, 2026.

In line with this earnings forecast, the Group plans to pay a dividend of ¥17 per share for the fiscal year ending December 31, 2026.

(Unit: ¥ billion)

| (¥ billion) | FY2022 Actual |

FY2023 Actual |

FY2024 Actual |

FY2025 Actual |

FY2026 Forecast |

YoY |

|---|---|---|---|---|---|---|

| Revenue | 1,309.0 | 1,442.6 | 1,638.7 | 1,774.2 | 1,920.0 | +8.2% |

| Adjusted Operating Profit | 140.8 | 181.5 | 199.6 | 274.9 | Growth rate disclosed | c.+10% |

| Operating Profit | 111.9 | 168.7 | 186.2 | 257.1 | 283.0 | +10.1% |

| Operating Margin | 8.5% | 11.7% | 11.4% | 14.5% | 14.7% | +0.2pt |

| Profit Attributable to Owners of Parent | 79.4 | 118.5 | 125.9 | 179.8 | 198.0 | +10.1% |

| Adjusted EPS (¥) | 45.4 | 57.6 | 60.4 | 86.0 | Growth rate disclosed | c.+10% |

| EPS (¥) | 33.8 | 50.4 | 53.6 | 76.7 | 85.3 | +11.4% |

| Annual Dividend (¥) | 11.0 | 14.0 | 15.0 | 16.0 | 17.0 | +1.0 |

*FY2022 figures represent profit attributable to owners of the parent from continuing operations. FY2023–FY2025 actuals and the FY2026 forecast represent profit attributable to owners of the parent.