Font Size

1. Front Cover

Good afternoon. I’m Masayoshi Nakamura, the Lead Independent Director of Nippon Paint Holdings.

I heard that most of the people here today also attended our small meeting held last year. Let me start with telling you a little about myself since I am meeting some of the attendants for the first time.

2. Profile of Independent Director

After graduating from college in 1977, I joined Mitsubishi Bank, Ltd. I left the bank after five years and returned to school. Then, I moved to Lehman Brothers and remained there for 15 years from 1984, including positions in Tokyo and New York. I subsequently was at Morgan Stanley for five years from 1999. From 2004 and onwards, I served as the Executive Officer with concurrent responsibilities for the securities business and the investment banking business at the Mitsubishi UFJ Financial Group and the Head of the Investment Banking Division of Mitsubishi UFJ Securities Company. In April 2010, I launched Mitsubishi UFJ Morgan Stanley Securities, which is a joint venture between Morgan Stanley Tokyo and Mitsubishi UFJ Securities. I started my own business in 2012 and have been working on my own since then.

The focus of my business activities has not changed after I became independent and I act as an advisor to customers concerning capital and M&A markets. It was around the spring of 2017, some five years after I started my own business, that I had an opportunity to meet Mr. Goh Hup Jin, the major shareholder of the Nippon Paint Group. I remember we started exchanging views within moments of meeting about the concept of Maximization of Shareholder Value (MSV). MSV is the concept I have come to embrace through my many years in the capital markets. It struck me then that Mr. Goh is another person who thinks the same way as I do. Since then we continued to exchange opinions occasionally.

At the General Meeting of Shareholders in March 2018, many of the members of the Board of Directors of NPHD were replaced. I was elected an Independent Director at this shareholders meeting and this is my fifth year. During those five years, I became the Lead Independent Director with NPHD’s shift to a Company with Three Committees (Nominating, Compensation and Audit) in March 2020, and have served as the Board Chair since April 2021, when NPHD adopted a Co-President structure.

3. Main Questions from Investors

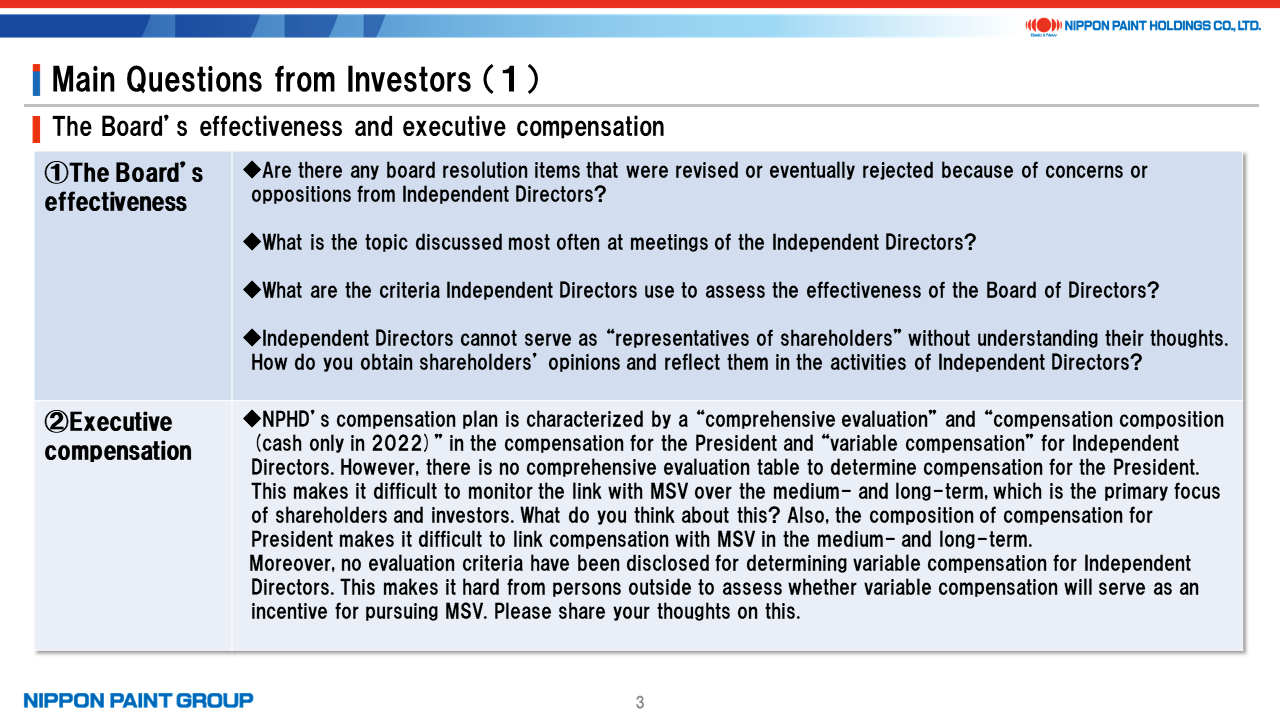

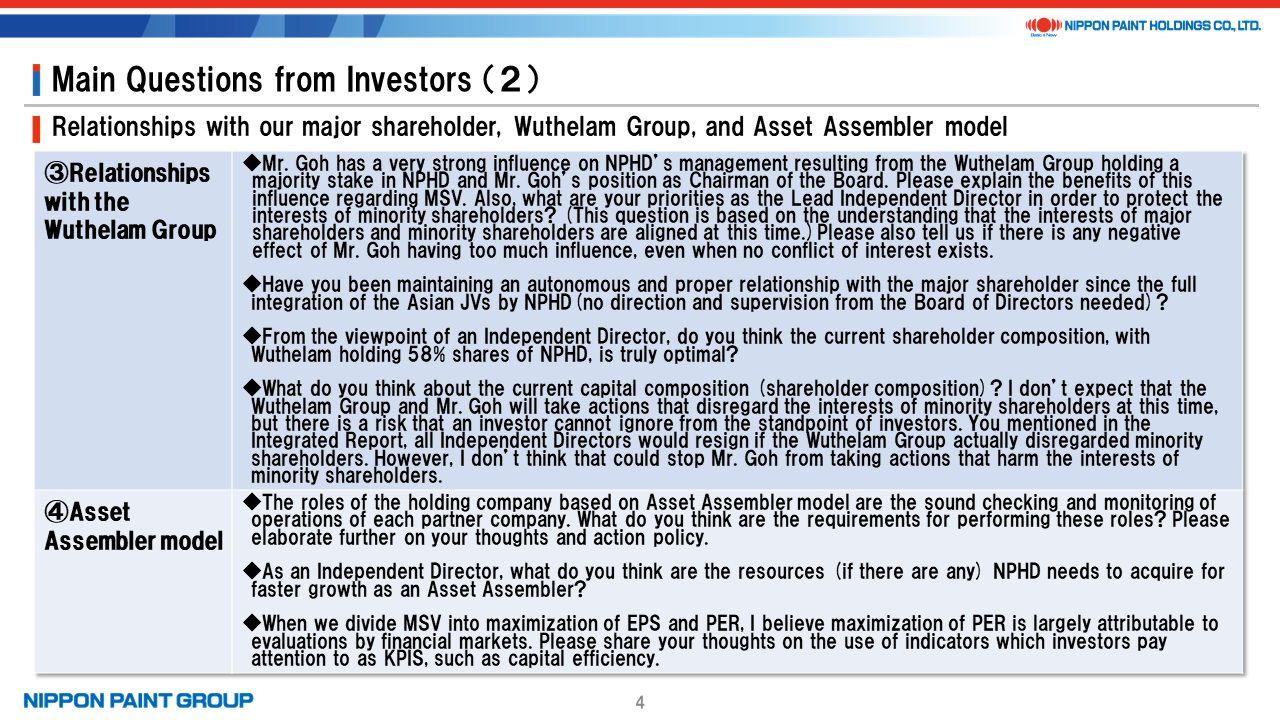

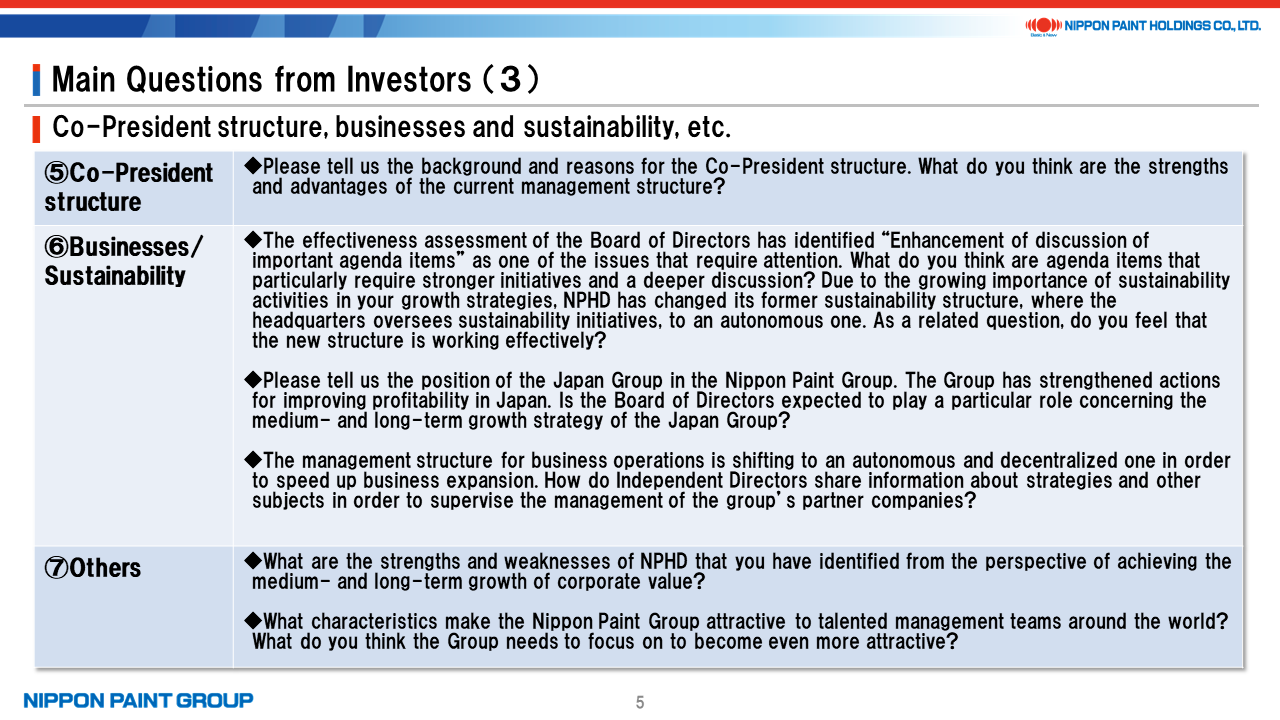

For today’s small investor meeting, we received many questions based on the Integrated Report of NPHD that was released at the end of August. The questions from investors have been categorized by topics: the effectiveness of the Board of Directors; executive compensation; relationship with the major shareholder; Asset Assembler model; the Co-President structure; businesses and sustainability; and other subjects.

We received questions about various aspects of executive compensation. I will talk about this topic first, followed by a question and answer session, and then answer questions on other topics as long as time allows.

The executive compensation part of the Integrated Report has a dialogue between Mr. Tsutsui, the Compensation Committee Chairperson, and me. The key points of the dialogue elaborate on the change in our thoughts on compensation from the period before the full integration of the Asian JVs to the period after the completion of the transaction leading up to the adoption of the Co-President structure. The dialogue also includes our discussions about the determination of compensation for the Co-Presidents based on a comprehensive evaluation. The Compensation Committee Report section explains the composition of our executive compensation.

The most important objective of today’s small investor meeting is to provide an explanation on the following two points. Firstly, what exactly the comprehensive evaluation process is? This year we adopted this process to replace the compensation based on the formula, which was described in the Annual Securities Report in prior years and had an excellent reputation among investors for the clarity of evaluation criteria. Secondly, why the composition of the Co-Presidents’ compensation was changed to an all-cash basis in FY2022. Our compensation plan previously was comprised of short-term incentives (STI) as performance-linked compensation determined based on a formula and long-term incentives (LTI), which is restricted stock compensation, and how did our compensation plan change? I would like to answer these questions.

The Board of Directors meetings of NPHD are operated with an emphasis on fairness and transparency. We explained the comprehensive evaluation and the composition of executive compensation in the Integrated Report. But I would like to go into more details about these topics today and your comments and feedback are welcome.

Compensation for the Co-Presidents and the Executive Officers is determined by the Compensation Committee and compensation for the Global Key Persons (GKP), who are the leading management of our group partner companies, by the Co-Presidents. To determine the compensation for GKP, the Co-Presidents evaluate their performance and report the results to the Compensation Committee or the Board of Directors.

Let me first explain the background for adopting this evaluation process. The Compensation Committee positions the evaluation of GKP and determination of their compensation as one of the important points for evaluating the Co-Presidents. These evaluations of GKP take into consideration the circumstances and characteristics of each country. Since the Nippon Paint Group’s management is based on autonomy of management and trust with each partner company, the basic assumption is that evaluations of GKP by the Co-Presidents should be aligned with recognition of the Directors. We maintain day-to-day communication with GKP for listening to their voices.

Now, I will explain the results of the comprehensive evaluation of the Co-Presidents in FY2021 based on this evaluation process. The evaluation criteria for the Co-Presidents include improving earnings in the Japanese and overseas businesses, establishing a sound stance in the stock market, risk management in the Nippon Paint Group, progress with the M&A strategy, which is the key growth pillar of our Group, the transformation of our corporate culture and management structure, and strengthening the governance structure and the internal control system. We concluded that the Co-Presidents had significantly accomplishments regarding all of these criteria.

The most significant achievement of the Co-President structure in FY2021 was that the Co-Presidents successfully achieved change in our strategic goals to respond to the rapidly changing business environment. With the targets in the Medium-Term Plan (FY2021-2023) announced in March 2021 unchanged, the Co-Presidents took actions that minimized the impact of supply chain disruptions caused by the pandemic, drastically reduced expenses at NPHD, the holding company, and revised the planned construction of the Shinagawa Head Office. As the result of their strategic initiatives, we believe that only NPHD and Sherwin-Williams, of all our major competitors, have basically maintained their PERs, which is included in the quantitative evaluation for the Co-Presidents. Of course, the Directors perform a comprehensive evaluation from multiple aspects by incorporating overall earnings and balance sheet management. Based on the results of these evaluations, the Compensation Committee made a final decision on compensation for the Co-Presidents.

In FY2021 after the adoption of the Co-President structure in April, members of the Compensation Committee examined the compensation structure under the new management structure in June and determined the compensation policy for the Co-Presidents. From August to November, we collected information and carried out deliberations for evaluating the Co-Presidents. We concluded compensation for the Co-Presidents for FY2022 in December 2021. In FY2022, concurrently with the determination of the Directors’ compensation after the General Meeting of Shareholders in March, the Compensation Committee and the Nomination Committee jointly held discussions about the February results of evaluations for GKP conducted by the Co-Presidents.

For evaluating GKP, succession plans are one of the most important factors. In addition to their contribution to business growth, we consider the expectations for future performance depending on their careers and development of potential successor as essential factors. There are cases in which the management team can develop their own skills by nurturing successors. On the other hand, we see many cases in which a company’s growth slows down as a result of failing to develop successors. We carry out evaluations on succession planning from time to time. We also evaluate the succession planning activities of the Co-Presidents in the same way.

This is my supplementary explanation of the evaluation and determination processes applied by the Compensation Committee that are designed to motivate the Co-Presidents, Executive Officers, and GKP.

However, we believe that compensation must reflect a broad range of trends and not be based solely on our own logic. We use benchmarking to avoid cases where we highly praise an individual but do not provide appropriate compensation or we give an individual excessive compensation that differs greatly from the generally accepted level.

The Compensation Committee constantly conduct research and analysis about trends and benchmarking of CEO’s compensation levels and composition in broad sectors around the world. Those studies are not limited to paint manufacturers with which we compete head-on in global markets. As a result, we are aware that compensation plan in which stock-based compensation accounts for a large proportion is not yet common among Japanese companies although the concept of short-term and long-term incentives has become established.

The final decision on compensation for the Co-Presidents is made by taking into consideration the results of benchmarking, as well as their performance. The governance dialogue in the Integrated Report provides a thorough explanation about how the comprehensive evaluation is performed. I took this opportunity to provide a supplementary explanation for the sake of transparency. However, my explanations earlier have not answered the question of why we decided to pay compensation for the Co-Presidents entirely in cash even though stock-based compensation is included in compensation for CEO-level executives of leading paint manufacturers in the US and Europe, which are the comparables of our analysis.

Based on Asset Assembler model we encourage every partner company to pursue autonomous growth. DuluxGroup used to have the stock-based compensation program for senior executives before joining our group as a partner company. After this type of compensation ended, some of the senior executives said they were comfortable about it while others have purchased NPHD stock with their own money.

The Compensation Committee’s interpretation of stock-based compensation is that this type of compensation forces the recipients to hold the stock of their company as part of compensation. One of the measures for designing compensation at NPHD is to rigorously examine the merits and demerits of stock-based compensation. There are various reasons but our conclusion at this time in the second year of the Co-President structure is that all cash compensation will contribute more to MSV. We will naturally need to adjust the compensation plan as we shift to a different phase of business operations and stage of growth. Opinions and comments of investors will be highly appreciated as reference for making appropriate adjustments.

Although the Co-Presidents’ compensation is paid entirely in cash, both hold NPHD stock. The issue we are facing now is whether or not we should impose stock-based compensation on the management team of NPHD in order to align their interests with those of investors and shareholders. The focus of this discussion is how to arrive at a conclusion.

Compensation involving stock is more complicated than all cash compensation. For example, there is a risk of a sharp drop in our stock price due to an economic slump, such as the collapse of the IT bubble around 2000 and the global financial crisis that started in 2008. As a result, the question we have now is whether stock-based compensation will really raise the motivation of recipients.

To explain the background for our decision to pay compensation for the Co-Presidents entirely in cash, the process of deliberations for determining Mr. Wee’s compensation is provided as an example in the Integrated Report. Mr. Wee was the Deputy President of NPHD and the CEO of the Nipsea Group. He made an enormous contribution to growth and earnings of the Nippon Paint Group prior to his appointment as the Co-President of NPHD. His compensation has consistently been paid entirely in cash. If we changed this compensation structure and paid the increase in compensation from the previous year in stock, there was a possibility that Mr. Wee’s motivation would not increase. Considering this, we decided the optimal compensation for the Co-Presidents in FY2022 was all cash compensation as the two Co-Presidents work together to pursue MSV.

The biggest governance challenge of the Nippon Paint Group is whether the management team can continue to boldly take risks in a timely and appropriate manner in the pursuit of MSV. Compensation for the management team including the Co-Presidents is the critical element of the structure to address this challenge. Compensation for the Co-Presidents for FY2022 was determined after going through the deliberation process I just explained. Let me reiterate that we have not made any decision about whether to continue the current compensation plan for FY2023 and afterward. What we must keep in mind is how we make changes with flexibility. Your valuable opinions and feedback are highly appreciated.