Released March 16, 2022

Nippon Paint Group Medium-Term Plan Progress

Outline of Medium-Term Plan (FY2021-2023) Progress

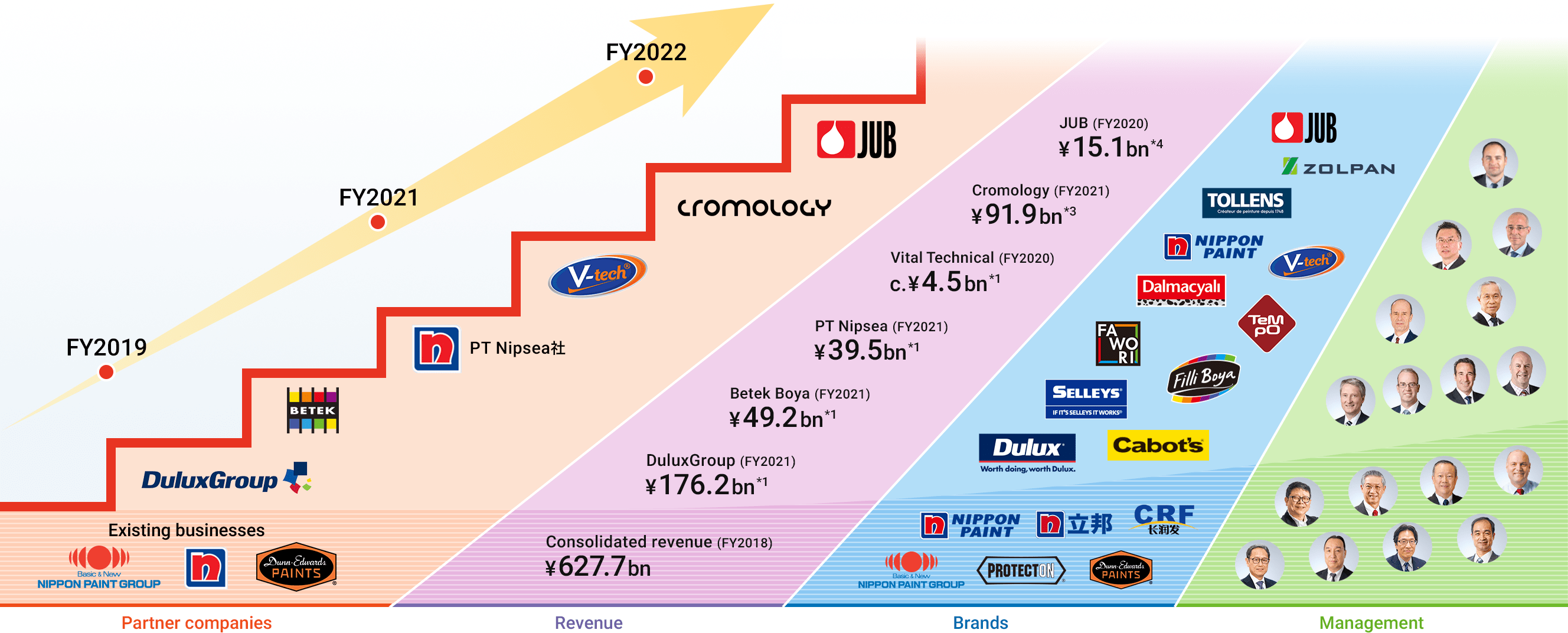

Year 1 of Medium-Term Plan provided the foundation for our "Asset Assembler" model

which combines strong organic and M&A growth.

We will continue to fuel our insatiable appetite for medium- and long-term growth.

Numerous corporate actions post Co-President setup

Aggressively pursue growth in paint and adjacency arena M&A, while also driving autonomous growth of existing Group partner companies*.

Established the basis for sustainable growth with small headquarters at the holding company and with reinforced governance.

Delivered strong revenue growth despite the pandemic

The strength of our business model is predicated on high market share in each region with emphasis on autonomy and accountability.

Expect to achieve Year 3 revenue target of 1,100 billion yen one year early.

Achieved effective operating profit growth despite challenging environment

Despite the impact of higher raw material prices and supply chain disruptions, achieved effective operating profit growth excluding one-off items with contributions from Indonesia, selling price increases, and significant savings in Head Office expenses compared to the initial plan.

Operating profit target for FY2023 unchanged

Well positioned to achieve Year 3 target of 140 billion yen operating profit and 45 yen EPS, driven by autonomous growth across the Group based on solid paint demand and market share gains, progress with selling price increases, and contributions from new acquisitions.

Asset Assembler

Nippon Paint is a unique Japan-based "Asset Assembler" with MSV as its sole mission

We have adopted a business model in which we, with a smaller headquarters at the holding company (NPHD), assemble assets focused on attractive markets in the paint and adjacency arena through M&A, while driving autonomous growth of the existing Group partner companies*, resulting in strong growth with limited risk. We call it the Asset Assembler model.

*Name of consolidated subsidiary companies of Nippon Paint Holdings

|

1. Focused on paint and adjacencies with significant market opportunities

-

Paint and adjacencies have significant growth opportunities, driven by population growth, per-capita GDP growth, and urbanization. We have considerable expertise and knowledge in these areas.

-

SAF*1(USD60.0 bn*2) and CC*3(USD71.5 bn*4) also have attractive market size.

|

|

2. Attractive risk-return profile of paint and adjacency arena

-

Strong brand and high market share raise entry barriers, leading to solidification of leading market position.

-

Paint and adjacencies markets are characterized by local production for local consumption, allowing for our autonomous and decentralized model to minimize PMI risk.

|

|

3. Japan domicile enhanced competitive strengths

-

Ability to finance at low interest rates in Japan, which has a stable currency and stable market, based on long-term relationships with banks.

-

Attractive Japanese capital markets, which have stable legal system and high liquidity in TSE.

|

|

4. An assembly of talented management and strong brands

-

Management of partner companies have deep understanding of market features in every region and are well versed into MSV, and can fully utilize their capabilities based on our autonomous and decentralized business model.

|

|

5. Advanced governance

-

Independent Directors comprise majority of the Board of Directors (8 out of 11 board members).

-

Ensuring protection of minority shareholders interests with MSV as a shared mission with our major shareholder.

|

*1 SAF: Sealants, Adhesives, Fillers

*2 Source: Fortune Business Insights

*3 CC: Construction Chemicals

*4 Source: ReportLinker

On top of strong organic growth, we assemble assets with strong brand and excellent management through M&A, effectuating accelerated growth with limited risk.

Sustainable Growth Model as Asset Assembler

The key element of this model is that excellent management teams pursue autonomous growth in the Nippon Paint Group and exploit the technological strengths, distribution networks, purchasing capabilities, and financing capabilities of the Nippon Paint Group platform, rather than relying on initiatives of the headquarters. This will allow us to accumulate expertise in various areas and generate synergies as well as to attract new partners to the Nippon Paint Group.

By focusing on the paint and adjacencies markets, which are growth markets with the ability to generate sustainable earnings and cash, the Asset Assembler model allows us to accelerate growth with limited PMI (Post Merger Integration) risk involving M&A.

*1 On a segment basis (after elimination of intersegment transactions and after PPA)

*2 Exchange rate: MYR 1=JPY 26.55

*3 Exchange rate: EUR 1=JPY 132.79; Unaudited pro forma figures

*4 Exchange rate: EUR 1=JPY 131.05; The acquisition is scheduled for completion in 1H 2022

Strategy By Region And Business

FY2021-2022 Revenue/Growth Rate

FY2022-2023 Actions

|

NIPSEA China Decorative (DIY) Business

-

Enrich product lines and coating systems and extend channel coverage

-

Continuous brand building and upgrading

NIPSEA China Decorative (Project) Business

-

Expand new channels and diversify customer base

-

Optimize operational and organizational structure

|

|

DuluxGroup (Oceania)

-

Continue strong track record of growth in Oceania

Maintain a focus on core fundamentals, including consumer engagement,premium brands, and innovation

-

Drive meaningful growth in European decorative paints and specialty coatings markets by leveraging recent acquisitions including Cromology

|

|

Betek Boya (Turkey)

-

Increase revenue and market share mainly through multi-brand strategy

-

Meet needs of diverse customer base mainly through brand differentiation

-

Build next generation of dealers, determine sales targets for each city, and implement effective market penetration strategy

-

Improve profitability in ETICS (External Thermal Insulation Composite System) through effective price management

|

|

PT Nipsea (Indonesia)

-

Continue to invest in advertising to drive brand top-of-mind and preference

-

Drive wider distribution of CCM*1 machines, increase product penetration in all product segments, and widen geographical coverage

-

Establish new e-commerce channels and increase sales contribution from non-paint segments

|

|

Japan Business

-

Drive revenue recovery in all businesses (expect markets to start recovering from the pandemic)

-

Increase productivity by clarifying expenses and earnings and plan to reallocate HD expenses in May 2022)

-

Continue to make necessary investments while reviewing SG&A and other expenses

-

Increase selling prices in response to high raw material prices (plan to raise selling prices in industrial business in April 2022 and decorative business in May 2022)

|

|

Automotive Coatings Business

-

Develop process-saving and low-temperature baking paint and launch anti-viral and anti-bacterial automobile interior coatings

-

Shifted from sale of paints for films to sale of painted films, expanding marketing outreach to outside Japan

-

Achieve growth in China by broadening product lines to boost sales and expanding business with emerging EV manufacturers

-

Become more competitive and expand business operations in electrodepositions segment globally

|

|

Paint Related Business

-

NIPSEA: Aim for rapid growth of paint related business and explore M&A opportunities that can accelerate growth

-

DuluxGroup: Maintain and accelerate Selleys*2 business growth in Oceania and Asia and explore entry into adjacencies market in Europe

-

Betek Boya: Differentiate from competition in ETICS*3 segment and introduce innovative services

|

*1: Computerized Colour Matching

*2: Brand for adjacencies products such as adhesives and sealants

*3: External Thermal Insulation Composite System

Sustainability Strategy

Progress & Further Plan of Materiality

Materiality (Relevant SDGs)

Progress

Further plan

Progress

-

Endorsed the TCFD final report recommendations and commenced disclosure in accordance with the framework

-

Calculated the potential financial impact of a carbon tax

-

Agreed global target for GHG emissions reduction*1 via each partner company developing targets that meet or exceed local government targets

-

Calculated Scope 3 GHG emissions*2

|

Further plan

-

Identify each partner company's top climate change risks and opportunities (high level scan) and potential actions

-

Identify each partner company's carbon reduction action plans and develop consolidated group view (H1 2022)

-

Agree objectives for common priority focus areas (e.g. energy efficiency, renewable electricity sourcing, vehicle fleet replacement) and implement

|

Resources and environment

Progress

-

Developed and disclose global policy statement for resources and environment (e.g. waste and effective use of resources, water)

|

Further plan

-

Identify each partner company's top resources and environment impacts, improvement priorities, and performance measures

-

Agree common priority focus areas (e.g. waste reduction) and objectives for 2022/2023 and implement

|

Safe people and operations

Progress

-

Developed global policy statement for safe people and operations (e.g. occupational safety and health)

|

Further plan

-

Identify each partner company's top safety risks, improvement priorities, and performance measures

-

Agree common priority focus areas (e.g. fire and fatality prevention) and objectives for 2022/2023 and implement

|

Progress

-

Confirmed the difference of the situation by each country and region

-

Disclosed the educational programs on a global basis

|

Further plan

-

Formulation of human rights policy

-

Implementation of human rights risk assessment

-

Global data aggregation for the human capital management disclosure

|

Progress

-

Established "NIPPON PAINT Group Global Outreach Program" as common framework followed NIPSEA CSR

-

NIPSEA established the concept "Colouring Lives" to have a bigger impact for the whole CSR activities as a group

|

Further plan

-

Promote quantification of activities

-

Promote CSR activities and data aggregation under the NIPSEA's concept "Colouring Lives" globally

|

Innovation for a sustainable future

Progress

-

Aggregated the sustainable products globally in 2021

-

Developed the Anti-Viral Paint Products across the group

-

Promoted open innovation with several 3rd parties

-

Initiatives regarding Chemicals of concern/LCA*3 in some companies

|

Further plan

-

Define the sustainable product

-

Develop and implement Green Design Review*4

-

Formulate strategy and roadmap

-

Strengthen the control of Chemicals of concern

-

Develop and leverage LCA*3 capability

|

*1: Scope1 & 2; intensity basis

*2: Disclosed Scope 3 GHG emissions from our operations in Japan in the Integrated Report

*3: Life Cycle Assessment: A method of quantifying the environmental impacts across the entire life cycle of a product

*4: Our unique framework that integrates the sustainability perspective in product development

M&A Strategy

Continue to pursue aggressive M&A strategy by leveraging our autonomous and decentralized business model

Our Asset Assembler model is not based on global standardization and common cost reduction programs, but rather pursues autonomous growth by assembling excellent companies with potential for a sustainable EPS contribution. We encourage collaborations with existing Group partner companies around the world and allow the use of financial resources provided by NPHD. We believe this is the right model to create medium- and long-term value in the paint and adjacencies businesses, which are characterized by local production for local consumption.

Targets

① Business segments: Paint(decorative/industrial) and adjacencies

② Geography: Not limited

③ Potential targets: Strong corporate/product, brand and excellent management team

① Fundamentals of paint and adjacencies markets e.g. population growth and urbanization create enormous growth opportunities

② No restrictions in terms of target locations as long as acquisition contributes to MSV. Distant location to be carefully examined

③ Continue to assemble assets leveraging strengths of our autonomous and decentralized business model

Our Strengths

① Financial soundness

② Ability to finance in Japan, with stable currency and stable market

③ Full access to the Nippon Paint Group’s platform

④ Excellent management teams enabling autonomous and decentralized business model

① Stable cash generating ability and strong financial position

② Low interest rate borrowings, safety and liquidity of the stock market

③ Sharing expertise, products, and technologies within the Group

④ Minimize the PMI risk

Financial Discipline

① Contribution to EPS

② ROIC*1>WACC*2

③ Sufficient leverage capacity

④ Debt financing prioritized; equity-based capital raising remains an option

① Aim to achieve EPS accretion in Year 1 after acquisition

② Take capital efficiency into consideration

③ Secure financial soundness to prepare for future M&As

④ EPS accretion also a must in rare case of equity financing

*1: Return on invested capital (after one-off expenses)

*2: Weighted average cost of capital

Related Materials of Nippon Paint Group Medium-Term Plan Progress

Links to related pages